Profile

Legal Structure

Masood Fabrics Limited (‘Masood Fabrics’ or ‘The Company’) was incorporated in 1998, as a public unlisted limited company.

Background

The Company was a venture of the Mahmood Group, which was originally established in 1935. Starting with the tannery business, the group now has a

presence in the complete cotton chain (growing to finished products), tanneries, real estate, and food. Masood Fabric is now part of the Masood-Roomi group, which was

formed in Apr'21

Operations

The Company is primarily engaged in the manufacturing and sale of greige fabric and yarn with a current operating capacity of 32,880 spindles and 260 looms respectively. It also has a significant investment portfolio and participates in the equity market. The Company generates 10.9 MW of combined power through captive generators and solar capacity. The registered head office of the Company is situated at 5 - Officers Colony, Multan.

Ownership

Ownership Structure

The ownership of the Company rests with the family of Mr. Khawaja Jalaluddin Roomi, including his wife, sons and

sisters. The major shareholding of the Company is owned by Mr. Khawaja Jalaluddin Roomi which is 77.28%, while the remaining ~22.72% is distributed among family members.

Stability

A clear and organized shareholding structure among family members, coupled with a well-established succession plan, reinforces the organization's stability and resilience. However, the establishment of a family constitution will enhance the stability and ownership profile of the Company.

Business Acumen

Mr. Khawaja Jalaluddin Roomi is a graduate with over 30 years of extensive experience. He has successfully led various government, semi-government, and public limited companies, developing strong expertise and business acumen. His vast knowledge and leadership capabilities equip him to effectively navigate and sustain any future challenges.

Financial Strength

Masood Fabric is a part of the Masood-Roomi Group of Companies. The sponsoring family has two other textile Companies; Roomi Fabric Limited, and Masood Apparels, and two holding Companies, Masood Holding and Roomi Holding. This indicates sponsors’ ability to provide support if the need

arise.

Governance

Board Structure

The board consists of five members from the sponsoring family. Mr. Khawaja Jalaluddin Roomi holds the positions of Chairman and CEO, while Ms. Humaira Jalaluddin and Mr. Najam-ud-Din Roomi serve as board directors. The board lacks independent oversight and the inclusion of independent directors will augment the governance framework of the Company.

Members’ Profile

Mr. Khawaja Jalaluddin Roomi is the Chairperson of the Company. He previously served as the Chairman-Management Board at Nishtar Medical College, Chairman at Multan Dry Port Trust and is currently heading Jalaluddin Roomi Foundation. Mr. Najam ud Din Roomi is the director of Masood Roomi Group and serves as independent director in Arif Habib Corp Limited. The directors’ expertise in various stages of the textile value chain leads to a

good skill mix.

Board Effectiveness

The total number of meetings held during the year was four, which were attended by all of the members. High attendance bodes well for board

effectiveness. No board committees are in place to assist the Board and its establishment will enhance the Company's governance profile

Financial Transparency

Crowe Hussain Chaudhry & Co. Chartered Accountants, who are categorized in category ’A’ by the SBP and have a satisfactory QCR rating by

ICAP, were the external auditors of the company. They have expressed an unqualified opinion on the company's financial statements for the year ending June 30, 2024.

Management

Organizational Structure

The organizational structure follows a hierarchical model, ensuring clear authority and accountability. The Chairman and Board of Directors provide strategic oversight, while the CEO manages overall operations, supported by the CFO, who oversees Taxation, HR & Admin, IT & ERP, and Finance. An independent Audit function ensures compliance and governance. Key business functions like Import, Purchase, Export, and Marketing are structured under HR & Admin and Finance, promoting operational efficiency. While this structure strengthens financial control, centralizing multiple functions under the CFO may slow decision-making. A more decentralized leadership approach could enhance agility and responsiveness.

Management Team

Mr. Khawaja Jalal-ud-Din Roomi, the company's CEO, is a graduate with over 30 years of extensive experience in leading government, semi-government, and public limited companies. He also serves on the board of Adamjee Insurance Company Limited. A team of professionals across various subdivisions, supports the top management to ensure efficient reporting and operations.

Effectiveness

Formal management meetings are conducted separately for each group company, chaired by Mr. Khawaja Jalal-ud-Din Roomi, with detailed minutes duly recorded. Currently, no management committees support the management team; however, their establishment would further strengthen the company's management framework.

MIS

Various MIS reports are generated and submitted to senior management to provide insights into monthly operations. These reports include Closing Stock and Finished Goods, Doubling Production, Cotton Reconciliation, Yield Analysis, and Raw Material & Work-in-Progress reports.

Control Environment

The Company deployed Oracle as an ERP solution in 2014. The group is currently operating Oracle R12, which has been customized by KPMG

Taseer Hadi & Co. Chartered Accountants. The operational modules include (i) Payable, (ii) Receivable, (iii) Inventory, (iv) Procurement, (v) Order Management, (vi) General Ledger, (vii) Fixed Assets, and (viii) Cash Management. Internal systems and controls, while integrating the business functions of the company, help the management in decision-making by collecting information timely. The in-house internal audit department is reportable to the board of directors.

Business Risk

Industry Dynamics

The textile exports of the country reached USD

16.7bln in FY24, a slight increase from USD 16.5bln in the previous year,

reflecting a growth of 0.93% YoY. The highest contribution came from the

composite and garments segment at USD 9.1bln, followed by the weaving segment

at USD 6.5bln and the spinning segment at USD 1.0bln. During 6MFY25, the

textile exports stood at USD 9.1bln. In FY25, the transition from the final tax

regime to the normal tax regime is set to impact the profitability matrix of

export-oriented units, with a 29% tax on profits and a super tax of up to 10%.

The consistent decline in policy rates over the last two quarters, along with

the anticipation of further reductions, is expected to provide a cushion in the

financial metrics of the industry

Relative Position

The Company has an operating capacity of 32,880 spindles and 260 looms respectively. Considering the operating capacity, the relative position of the Company is considered adequate and the Company is a low to mid-tier player in the textile industry.

Revenues

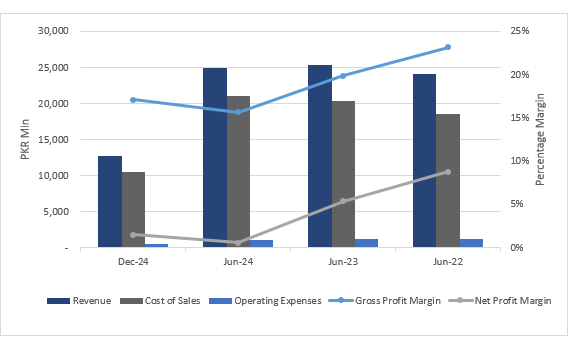

The company generates a

major portion of its revenue from local and export sales. During FY24, the

company's topline recorded a marginal decline to stand at PKR 24.9bln (FY23: PKR

25.3bln) attributable to the adverse pricing dynamics and shortage of yarn

demand. The sales mix tilted toward the export market as export sales (including indirect exports) recorded a decrease to PKR 21.4bln (FY23: PKR 22.4bln)

comprising the sale of yarn and fabric. The company's local sales increased to

PKR 3.7bln (FY23: PKR 3.4bln). The company operates in two key segments:

spinning and weaving. While both contribute to the overall performance, weaving

plays a more significant role in driving the Company’s topline. The top 4 export destinations for the Company, which

account for almost 60% of total export sales in terms of volume, are China, the Netherlands, Italy, Germany, and the USA. During 6MFY25, the

company’s revenue base remained stagnant to stand at PKR 12.7bln

Margins

During

FY24, the gross margin reflected a decline at 15.7% (FY23: 19.9%) followed by a

hike in production cost. Consequently, the operating margin witnessed a decline

to 11.4% (FY23: 15.1%) The Company’s finance cost increased manifold to PKR

3.6bln (FY23: PKR 2.2bln). The net profit of the Company saw a sizeable decline

to stand at PKR 158mln (FY23: PKR 1.4bln). Consequently, the net profit margin

stood at 0.6% (FY23: 5.4%). The Company's non-operating income sizably increased and stood at PKR 1.5bln (FY23: PKR 845mln), supplementing the profitability. During 6MFY25, the company's gross profit margin

and net profit margin stood at 17.1% and 1.5%, respectively.

Sustainability

During FY24, the Company has executed CAPEX and installed ~9MW of solar capacity to mitigate the escalating energy cost risk. Moreover, the Company has executed BMR and added 240 spindles to its operating capacity. No further CAPEX is expected going forward, as the existing infrastructure and resources are deemed sufficient to support the company's operational and strategic objectives.

Financial Risk

Working capital

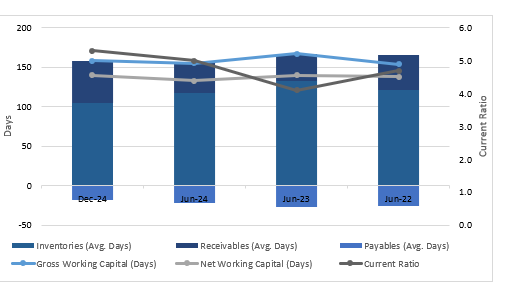

At end-Jun24, the company's net working capital

days declined to 133 days (end-June 23: 140 days) owing to a decline in the

inventory days recorded at 117 days (end-June 23: 132 days). The company's

short-term trade leverage stood at 0.5% (end-Jun23: 0.5%) due to a decrease in

trade assets recorded at PKR 11.9bln (end-Jun23: PKR 12.3bln). At end-Dec24,

the net working capital days stood at 140 days (FY23: 140 days).

Coverages

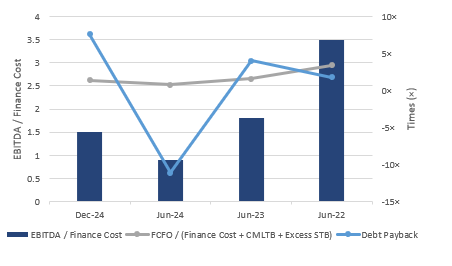

At

end-Jun24, the company's free cash flows from operations decreased to PKR 2.9bln

(end-Jun23: PKR 3.6bln). The company's interest coverage ratio declined to 0.8x

(end-Jun23: 1.6x) and debt coverage to 0.6x (FY23: 1.1x). At end-Dec 24, the

company's interest coverage and debt coverage ratio each stood at 0.8x, with

FCFO clocking at PKR 1.7bln.

Capitalization

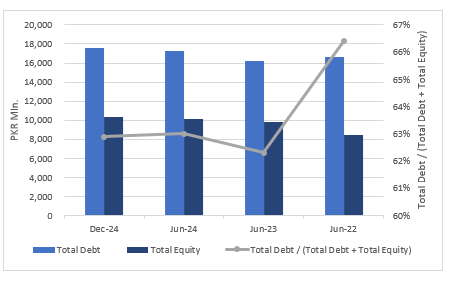

At end-Jun24, the company has a highly leveraged

capital structure. The company's leveraging inclined to 63.0% (end-Jun23: 62.3%). The company's equity base increased to PKR 10.1bln (end-Jun23: PKR

9.8bln). Total borrowings to stand at PKR 17.3bln (end-Jun23: PKR 16.1bln). At the end of Dec 24, the company's equity base stood at PKR 10.3bln. The company's

leveraging clocked in at 62.9%

|