Profile

Legal Structure

Ahmed Fine Textile Mills Limited ("AFTML" or "the Company") operates as a public unlisted Company under the repealed Companies Ordinance, 1984 (now Companies Act 2017).

Background

AFTML, established in 1989, has evolved into a leading player in the textile industry. Initially, focused solely on the manufacturing of yarn and fabric, the Company has significantly expanded its operations and now it operates as a composite unit. In addition to its core expertise in yarn and fabric production, the Company has diversified its product portfolio by venturing into the terry towel segment.

Operations

The Company boasts an annual production capacity of 83,820 spindles, 492 looms, and 39 terry looms. It operates with two state-of-the-art spinning units, located in Multan and Rahim Yar Khan, accompanied by a consolidated annual production capacity of 40.7 million kilograms of yarn, 110.5 million yards of greige fabric, and 3.9 million kilograms of terry towels. The Company’s weaving unit, situated in Multan, specializes in the production of greige fabric and high-quality export-grade towels. This manufacturing infrastructure enables the Company to meet both domestic and international demand efficiently.

Ownership

Ownership Structure

The Company is a business venture of the sponsors of a renowned business group, Fazal Group. The major shareholding (~84%) of the Company rests with Mian Rehman Naseem while the remaining stake (~16%) is owned by Mian Hussian Ahmad Fazal.

Stability

The Company’s ownership structure is expected to remain stable in the foreseeable future, as evidenced by the transfer of a significant stake to Mian Rehman Naseem, establishing a clear and structured line of succession. Moving forward, the transfer of the remaining shares to Mian Rehman Naseem is expected to culminate by the end of FY25, ensuring a seamless transition of ownership.

Business Acumen

Fazal Group has a longstanding history within the country's economy, further strengthened by its five decades of presence in the local textile industry. The group has weathered several economic cycles over the years, yet its growth has remained intact, enabling the sponsors to navigate the industry's volatility.

Financial Strength

The financial strength of the sponsoring group emanates from its one additional Company operating in the textile domain; Fazal Cloth Mills Limited with a topline of ~PKR 97bln. The strategic investments in the fertilizer and textile sectors at the group level depict the strong financial capacity of the sponsors to support the Company if needed.

Governance

Board Structure

The Company's board is dominated by the sponsoring family. The overall control of the board is vested with seven members, including the Chairman and the Chief Executive Officer. The inclusion of an independent oversight will enhance the governance framework of the Company.

Members’ Profile

The Chairman, Mr. Sheikh Naseem, brings over five decades of experience in the textile industry. He serves as the key decision-maker at Fazal Cloth Mills Limited and holds directorships at other group companies. Mr. Abdullah Amir Fazal has three years of experience in the textile industry and has been a member of the Company's board since 2019. Mr. Naveed Amer, who holds a Master's degree in Business Administration, has been associated with the Company for approximately twenty-six years. Mr. Haziq Fazal, Ms. Atiqa Hussain and Ms. Minahil Fazal have been serving on the Company's board since 2019.

Board Effectiveness

The Company has formed an Audit Committee to assist the board in addressing critical financial and regulatory matters. Additionally, the attendance of members at BOD meetings remained strong, with minutes meticulously recorded to capture key discussions and decisions.

Financial Transparency

To uphold high standards of transparency, the Company has an internal audit department in place that reports to the CEO. M/s Yousuf Adil & Co. Chartered Accountants have been appointed as the external auditors of the Company rated in "Category A" by the SBP panel of auditors. They expressed an unqualified opinion on the financial statements of the Company for the year ended June 2024.

Management

Organizational Structure

The management control of the Company vests with Fazal Group, through Mr. Rehman Naseem serving as the CEO of the Company. The Company's organizational

structure has been divided into five functional departments to ensure the smooth flow of operations.

Management Team

Mr. Rehman Naseem, the Chief Executive Officer, is a graduate of Columbia University and brings more than two decades of experience in the textile industry. The Company also benefits from a team of seasoned professionals with long-standing tenure, contributing to its sustainable growth prospects. Mr. Naveed Amer, serving as the Chief Financial Officer holds a master's degree in Business Administration and brings with him over three decades of experience in the textile industry.

Effectiveness

The management meetings are conducted on a periodic basis which ensures accountability. In addition to these scheduled meetings, ad-hoc meetings are held as needed to address specific bottlenecks and troubleshoot any operational challenges. This approach ensures that both routine oversight and urgent concerns are effectively managed.

MIS

For comprehensive reporting, the Company has implemented an Oracle-based Enterprise Resource Planning (ERP) system, which is regularly updated and includes various operational modules.

Control Environment

AFTML is accredited with various international certifications for compliance. The Company is following the latest Quality Assurance

Standards for yarn and fabric production. A few of the prominent certifications include ISO 9001, Lycra assured, and Fair Trade.

Business Risk

Industry Dynamics

Textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%.

Relative Position

AFTML falls in the mid-tier of the respective industry with a total production capacity of 83,820 spindles, 492 fabric looms and 39 towel looms.

Revenues

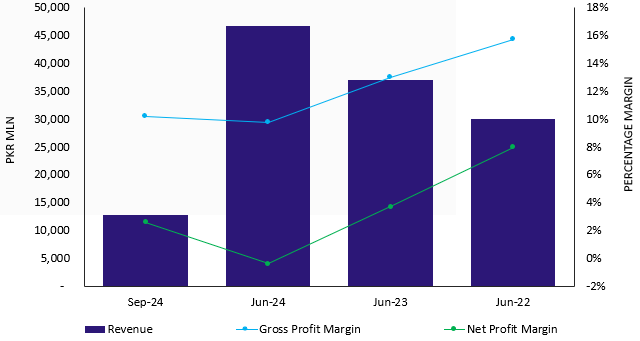

During FY24, the Company's topline exhibited remarkable growth reaching PKR 46.6bln (FY23: PKR 37.0bln) followed by a three-year CAGR of 16.3% from 2022 to 2024. The Company's sales mix remained largely the same. The export sales experienced an upswing (FY24: PKR 26.5bln; FY23: PKR 19.0bln), dominated by fabric sales, which constitute around 73% followed by towels and yarn. The Company's export destinations for all three segments (spinning, weaving, and towel) include Portugal, Singapore, Italy, Switzerland, Turkey, Romania, France, etc. The Company has established a stable customer base around the globe indicative of a low geographic concentration risk. The Company's top 20 client concentration for exports remained moderate, however, the long association of the Company with stable entities provides comfort. The local sales have a contribution of approximately 46.4% recorded at PKR 21.6bln (FY23: PKR 18.4bln). During 1QFY25, the Company's topline posted a sizeable improvement reported at PKR 12.8bln (1QFY24: PKR 11.8bln) indicating an uptick of 8.1% on a quarter-on-quarter basis.

Margins

During FY24, the Company's gross profit margin witnessed a dip at 9.8% (FY23: 13.0%) primarily due to a progression in raw material prices and escalated energy cost. The Company maintained its GP margin through strategic adjustments in the product mix towards higher-demand products such

as coarse yarn and grey fabric. The operating expenses surged by 36.3% on a year-on-year basis at PKR 1.3bln (FY23: PKR 979mln) concomitant with the inflationary trends. The Company's operating profit margin stood at 6.9% (FY23: 10.4%). The profit before interest and taxes was contracted to PKR 3.8bln (FY23: PKR 4.6bln) on the back of a slump in the exchange gain compared to the corresponding period. The higher interest rates resulted in a massive increase in the finance cost (FY24: PKR 3.6bln; FY23: PKR 2.7bln). Consequently, the Company's bottom line recorded a net loss of PKR 188mln against the net profitability of PKR 1.3bln in FY23. During 1QFY25, the Company's gross profit margin inched up to 10.2% (1QFY24: 12.4%) attributed to an improvement in the revenue base. The gradual decrease in the interest rates led to an uptick in the net profitability (1QFY25: PKR 336mln; 1QFY24: PKR 149mln) with the net profit margin of 2.6% (1QFY24: 1.3%)

Sustainability

In FY24, the Company resumed its expansion initiative, aiming to enhance its spinning production capacity by adding 50,000 spindles. This expansion was carried out in two phases and has now been completed. The Company has successfully installed a 3.5 megawatt solar power system which is currently operational. Further, the installation of a 7.5 megawatt solar is still under process with plans underway to install an additional 10 megawatt solar to curb the impact of escalated energy costs. In the coming years, the management plans to strategically invest in advanced laser printing technology over the coming years. This investment is aimed at enhancing production capabilities and enabling the Company to meet evolving market demand. The adoption of laser printing technology is expected to support innovation in product offerings, reduce costs, and strengthen the Company's competitive edge in the industry.

Financial Risk

Working capital

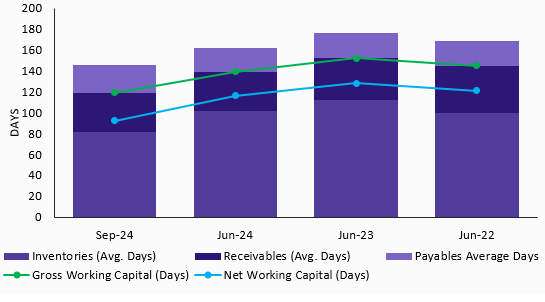

The Company's working capital cycle is a function of inventory days and trade receivables days for which the Company mainly relies on short-term borrowings. During 1QFY25, the net working capital cycle improved to 91 days (FY24: 115 days) attributed to a decline in the inventory cycle (1QFY25: 81 days; FY24: 102 days), however, the elevated payable cycle reflects that the delay in payments to the suppliers. The Company holds a limited borrowing capacity as illustrated by the short-term trade leverage reported at 27.8% (FY24: 27.5%).

Coverages

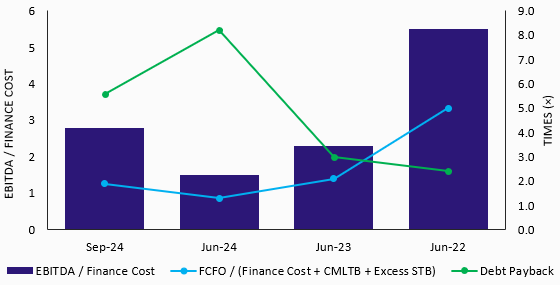

The dilution in PBT ultimately impacted the Company's Free Cash Flows from Operations (FCFO) reported at PKR 988mln (FY24: PKR 4.8bln). With the decrease in funding cost and FCFO, the Company's interest coverage exhibited a minute improvement and stood at 1.9x (FY24: 1.3x) whereas the core operating coverage remained largely the same at 1.0x (FY24: 0.9x). Going forward, the improvement in the coverages of the Company remains essential.

Capitalization

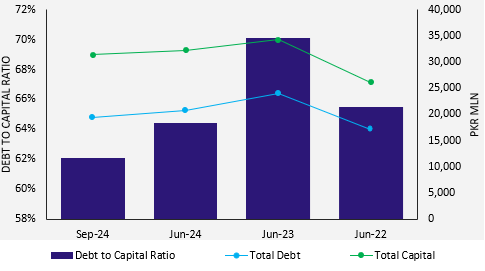

The Company's debt profile comprises subsidized borrowings by the State Bank of Pakistan (SBP) as well as conventional borrowings. The Company secured long-term subsidized loans specifically aimed at achieving the targeted production capacity in its spinning and towel segments. The Company has maintained a leveraged capital structure mainly dominated by short-term borrowings (STBs) to meet the extensive working capital requirements which account for 45.7% of the borrowing book. During 1QFY25, the total leveraging went down to 62.1 %, compared to 64.4% as of FY24. However, the Company’s equity base was enhanced to PKR 11.9bln (FY24: PKR 11.4bln), with an unappropriated profit of PKR 10.9bln, demonstrating the Company's ability to maintain its financial position despite the higher borrowing levels.

|