Profile

Legal Structure

Basfa Textile (Pvt.) Ltd, established in 2006, commenced commercial operations in 2008. The corporate office is situated at 20-KM Ferozepur Road,

Lahore.

Background

The company was founded by Mr. Jahangir Saleem, who was previously engaged in the car paint and chemical raisins business under Basfa Industries (Pvt.) Ltd. and Auto Coatings (Pvt.) Limited before entering the textile industry. The name "BASFA" is derived from the initials of his four sons: Mr. Babar Jahangir, Mr. Sajid Jahangir, Mr. Fahad Jahangir, and Mr. Ahmad Jahangir.

Operations

The Company specializes in the manufacturing and sale of viscose and cotton yarn, with a total production capacity of 60,156 spindles. Its product portfolio includes viscose yarn sold under the brand name “Super-Diamond” and cotton yarn under the brand name “Super-Gold.” The Company operates two production facilities: Unit 1, located at 36-KM Ferozepur Road, Lahore, with a capacity of 38,136 spindles, and Unit 2, situated at Feroz Watwan Road, Chandi Kot Stop, Sheikhupura, with a capacity of 22,020 spindles.

Ownership

Ownership Structure

The Jahangir Saleem family holds the controlling stake in the company. Mr. Babar Jahangir (Chairman/CEO) owns 44.40% of the shares, and Mr. Ahmed Jahangir and Mr. Fahad Jahangir hold 30.0% and 25.60% of the shares, respectively. Collectively, the Jahangir Saleem family owns 100% of the company’s shares, maintaining complete control over its operations.

Stability

BTPL has a strong and stable ownership structure, supported by a documented succession plan. Mr. Jahangir Saleem has distributed ownership among his sons, ensuring a clear and organized transition.

Business Acumen

Before the textile business, the sponsor’s primary business was car paints and chemical raisins used in the fibreglass industry and steel putty (a

product of the auto industry). Mr. Babar Jahangir has an overall working experience of 18 years. His innovative technological skills in the field of the textile sector bring

specialized and comprehensive knowledge to the board.

Financial Strength

As a single line of business, Basfa Textile's financial strength is considered adequate, with the sponsor offering financial support and commitment during times of need.

Governance

Board Structure

The Board of Directors, under the leadership of CEO/Chairman Mr. Babar Jahangir, consists of three members, including Directors, Mr. Ahmed

Jahangir and Mr. Fahad Jahangir. The inclusion of an independent director would strengthen the Company's governance framework.

Members’ Profile

Mr. Babar Jahangir, the Chairman and CEO of the Company, holds a UK graduation degree and has been associated with BASFA Textile for the past eighteen years. Additionally, Mr. Ahmad and Mr. Fahad Jahangir, both graduates from universities in the USA and the UK respectively, have been members of the board

for the past four years.

Board Effectiveness

The board is currently heading two committees (i) Audit Committee – who is primarily responsible for supervision of all matters related to audit and

finalization of financial accounts. The internal audit department is predominantly engaged in the operations of this committee (ii) Corporate performance and evaluation

committee – which is primarily responsible for recommending HR policies, succession planning of key management roles and monitoring key performance metrics.

Financial Transparency

HASNAIN ALI Chartered Accountants (QCR rated) are the external auditors of the Company. The firm holds a satisfactory Quality Control Review (QCR) rating. They expressed an unqualified opinion on the

Company’s annual financial statements for the year ended June 30, 2024.

Management

Organizational Structure

The company maintains a lean organizational structure, ensuring efficiency and effective communication across all levels. It operates with key departments, including (i) Accounting, (ii) Finance, (iii) HR, (iv) Technical (v) Operations, and Procurement. The Finance and Admin Managers report to the CFO, while the CFO, Marketing Manager, General Manager of Production, and General Manager of Auto Coro (Unit-2) report directly to the CEO.

Management Team

Mr. Babar Jahangir is the CEO of the Company, while Mr. Ahmed Jahangir and Mr. Fahad Jahangir hold Director positions, with Mr. Fahad Jahangir specifically overseeing the role of director commercial. Mr. Ahmed Jahangir oversees operations and finance-related matters. Mr. Abdul Basit, the company's CFO, is a Fellow Public Accountant and Fellow Cost and Management Accountant with nearly 32 years of experience, including 18 years with Basfa Textile (Pvt.) Ltd. Additionally, the General Manager of Marketing has 29 years of experience in the textile industry.

Effectiveness

The Company does not have formal management committees; however, top management frequently meets to discuss critical matters, assess daily operations, and review progress toward projected targets. Basfa Textile maintains an adequate IT infrastructure with appropriate controls and has been using QuickBooks – Accounting Edition since 2016 under a licensed setup for approximately 10 corporate users, supporting various operational modules, including Accounts Payable, Accounts Receivable, Inventory Management, Procurement, Order Management, General Ledger, Fixed Assets, and Cash Management.

MIS

Various MIS reports are prepared for the management to keep track of all operating activities. Daily reports are generated for the senior management, which helps

them in day-to-day decision-making. Apart from daily reporting, the management also receives a more detailed MIS on a monthly basis.

Control Environment

The Company utilizes intra-networking to connect all departments through a common network, with user-based controls ensuring secure access. Dedicated servers support structured data management and backup policies. To uphold a strong control environment, the Company has established an Audit Committee that ensures compliance with policies, enhances operational efficiency, and oversees the Internal Audit Department, which monitors operational performance, reinforces governance, and strengthens internal controls. The internal audit report is submitted directly to the Board of Directors (BOD).

Business Risk

Industry Dynamics

The textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. During 5MFY25, the textile exports stood at USD 7.6bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%. The consistent decline in policy rates over the last two quarters, along with the anticipation of further reductions, is expected to provide a cushion in the financial metrics of the industry.

Relative Position

The Company is categorized as a low to mid-tier player in the dedicated spinning industry, with an estimated production of 11.33 mln kgs of yarn.

Revenues

BIPL's

top-performing product is viscose yarn, followed by cotton yarn,

polyester-cotton yarn, and polyester-viscose yarn. As part of its profit-driven

business strategy, the Company has optimized its product mix by shifting

towards the production of finer yarn counts. This strategic shift has extended

the product lead conversion time while reducing total daily output due to the

processing requirements of finer yarn manufacturing. This resulted in a

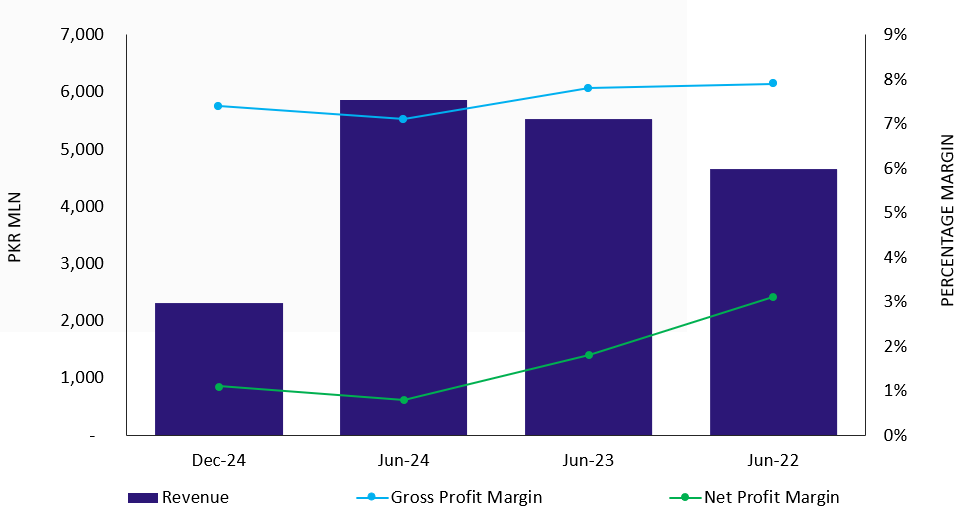

reduction in sales during 1HFY25 which stood at PKR 2,320mln (1HFY24: PKR

3,017mln, FY24: PKR 5,524mln).

Margins

The

margins of the Company have slightly increased mainly on the back of improved

product pricing during 1HFY25 in comparison with FY24 despite the increase in

operating expenses to sales ratio. In FY24, the gross profit stood at PKR 413mln (1HFY25: PKR 172mln). The net profit margin slightly improved to 1.1% in 1HFY25 in comparison with FY24 of 0.8%.

Sustainability

The Company's sponsors are exploring new investment avenues within the textile value chain to augment business sustainability. To manage energy costs and supplement its ~5.9-megawatt energy requirement, the Company has already installed a 2.1-megawatt solar power plant and is in the process of installing an additional 1.2-megawatt system.

Financial Risk

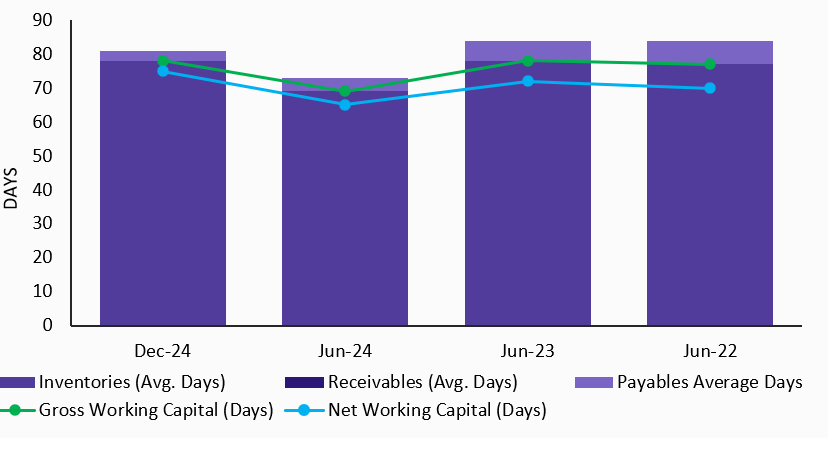

Working capital

In 1HFY25, net working capital days increased to 75 days from 65 days in FY24, mainly due to a change in the product mix, which was more focused on producing finer yarn counts. This reduced sales in monetary terms, resulting in a surge in inventory days. Overall, the Company effectively managed its working capital requirements, which were primarily met through short-term borrowings. The Company has a nil trade receivables balance, which supports its working capital cycle. As of 1HFY25, the Company has maintained short-term trade leverage at 23.6%, reflecting adequate borrowing capacity.

Coverages

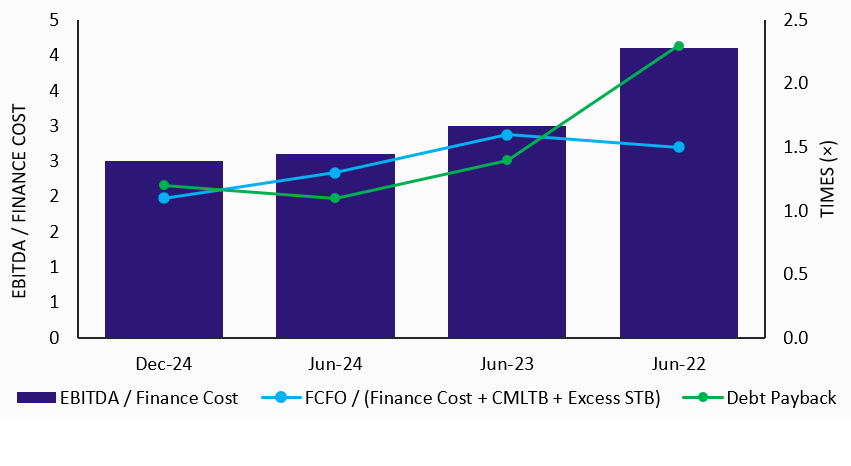

In FY24, FCFO stood at PKR 511mln (FY23: PKR 547mln), reflecting stable cash generation from core operations. The interest coverage ratio was 2.2x, while the operating coverage ratio stood at 1.3x, demonstrating the company’s ability to meet financial obligations. In 1HFY25, the interest coverage ratio remained largely stable at 2.1x, while the operating coverage ratio stood at 1.1x. The renewable energy initiatives are expected to generate cash savings and create a cushion in the cashflow management of the Company.

Capitalization

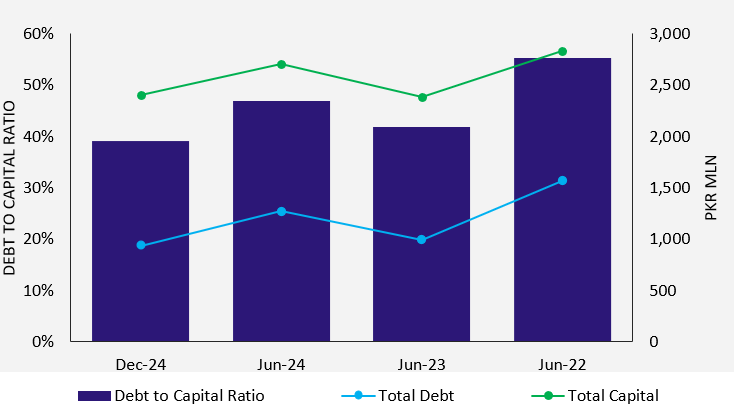

In 1HFY25, BTPL maintained a moderately leveraged capital structure; the leveraging ratio stood at 39.1% (FY24: 46.9%) improved mainly on the back of a reduction in short term borrowings from PKR 946mln in FY24 to PKR 690mln in 1HFY25. The long-term borrowings were also reduced to PKR 93mln as of 1HFY25 after some debt repayment. The management of the Company is committed to sustaining its current debt levels to maintain leveraging at an optimal level by funding future expansion mainly through equity. The equity base of the Company stood at PKR 1,462mln mainly supplemented by 917mln from unappropriated profits with no revaluation surplus depicting pure equity.

|