Profile

Structure

HBL Microfinance Bank Limited ("HBL MfB" or the "Bank") was incorporated in 2001 as a nationwide microfinance institution and obtained the Microfinance banking license from the State Bank of Pakistan in 2002.

Background

The Bank was founded as a structured transformation of the credit and savings section of the Aga Khan Rural Support Programme (AKRSP), a development initiative pioneering microfinance in Gilgit-Baltistan and Chitral since 1982.

Operations

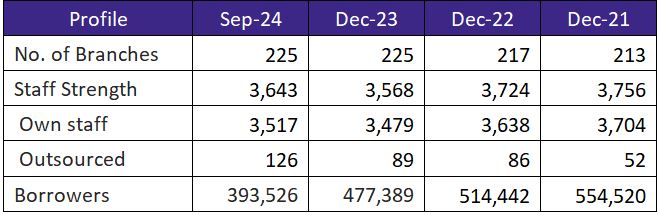

As of end-Sep24, the Bank operates 225 business locations, including branches and permanent booths (end-Dec23: 225), with its head office based in Islamabad. The Bank provides a diverse range of products and services for low-income wage earners and the self-employed, focusing on microlending segments such as Agriculture, Livestock, Micro-enterprise, Housing, Nano Loans, Solar Finance, and more.

Ownership

Ownership Structure

The Bank's ownership is primarily held by HBL with a stake of 89.38%, followed by the Aga Khan Agency for Microfinance (AKAM) at 6.37%, Aga Khan Rural Support Programme (AKRSP) at 2.36%, and Japan International Cooperation Agency (JICA) with 1.89%.

Stability

This ownership structure is expected to remain stable in the near term.

Business Acumen

The Aga Khan Development Network (AKDN), which sponsors HBL, AKAM, and AKRSP, is a group of agencies focused on development in areas such as environment, health, education, architecture, culture, microfinance, rural development, and disaster management. AKDN aims to improve the quality of life for underserved communities, mainly in Asia and Africa, by fostering self-reliance.

Financial Strength

The sponsor's business expertise is considered strong, with HBL, the direct sponsor, recognized as one of Pakistan's largest banks by deposits and advances. At end-Sep24, the HBL's deposit base stood at PKR 4.8tln, with equity at PKR 411bln.

Governance

Board Structure

The Board of Directors consists of eight members: four representatives from HBL, one from the Aga Khan Agency for Microfinance, one from the Aga Khan Rural Support Programme (AKRSP), and two from the Japan International Cooperation Agency.

Members’ Profile

The Board is chaired by Mr. Rayomond Kotwal, CFO of HBL, who has over 30 years of senior finance experience across various commercial banks. Each Board member brings significant expertise, with a majority possessing extensive banking experience, enhancing the Board's overall strength.

Ms. Maya Inayat Ismail brings over 25 years of experience in the financial services sector, with roles at HBL, HBL Microfinance Bank Ltd., and Global Securities Pakistan Ltd. She specializes in monitoring financial institutions, managing strategic partnerships, and strategy formulation. Ms. Ismail holds a Bachelor of Arts in Economics and International Relations from Smith College, Northampton (USA), and is an Accredited Mediator from the Centre for Effective Dispute Resolution, UK.

Mr. Abrar Ahmed Mir has over 30 years of experience, having worked with United Bank Limited, Citibank N.A., and ICI Pakistan, among others. He is currently HBL’s Chief Information & Transformation Officer. Mr. Mir holds an MBA from the Illinois Institute of Technology, a BE in Electronics Engineering from the College of Electrical and Mechanical Engineering, Pakistan, and completed the "Strategic Leadership in Inclusive Finance" course at Harvard Business School.

Ms. Sobia Chughtai brings 32 years of diversified experience in the financial sector. Currently serving as Portfolio Head Corporate Risk – Central at HBL, she has previously held key positions at Al Faysal Investment Bank Limited and Fauji Fertilizer Company. She holds an MBA from LUMS and a BSc in Electrical Engineering from UET, Lahore.

Mr. Zahir Riaz is a Partner at Orr, Dignam & Co. and leads the Islamabad office. With 42 years of experience, he specializes in corporate law, mergers & acquisitions, banking & finance, capital markets, construction, privatizations, and energy. He holds legal degrees from the London School of Economics, University of Cambridge, and is a qualified Barrister from Gray’s Inn, UK.

Ms. Rashna Minwalla has extensive experience in financial securities, derivatives, and equity broking, having worked at Elixir Securities Pakistan, JP Morgan Broking Pakistan, and other firms. She is currently the CEO & Director of The Fertility Clinic in Karachi. Ms. Minwalla holds a Masters in Finance from the London Business School and both a Masters and Bachelor's in Business Administration from the Institute of Business Administration, Karachi.

Mr. Tsuyoshi Hara is the Senior Representative for JICA Pakistan, with over 15 years of experience in managing development projects. He has worked at JICA and JBIC, specializing in infrastructure projects such as power, water, sanitation, and public-private partnerships. Mr. Hara holds a Bachelor's degree in Economics from Keio University, a Master's in Economics (specializing in Public-Private Partnerships) from Toyo University, Japan, and is a Ph.D. candidate in Public Policy and Public Administration at Florida State University.

Ms. Kate Perkins has 15+ years of experience in the financial services sector. She is currently the Investment Director at British International Investment plc, focusing on equity investments in Africa and South Asia, with a specialization in financial inclusion. Previously, Ms. Perkins worked at Nesta, Citigroup, and EY, where she qualified as a Chartered Accountant. She holds an MPhys degree in Physics from Oxford University.

Board Effectiveness

The Board has six committees: (i) Human Resource Committee, (ii) Risk & Compliance Committee, (iii) Audit Committee, (iv) Information Technology Committee, (v) Financial Inclusion & Sustainability Committee, and (vi) Board Remuneration Committee. In CY23, the Board held four meetings, with satisfactory attendance.

Transparency

KPMG Taser Hadi & Co. serves as the Bank’s external auditor and issued an unqualified opinion on the financial statements for the year ending December 31, 2023. The internal audit department reports directly to the Audit Committee.

Management

Organizational Structure

The Bank operates with a horizontally structured organization, comprising 11 departments that report directly to the Chief Executive Officer. Each reporting line and job description is clearly defined.

Management Team

Mr. Muhammad Amir Khan, the CEO and President, has been with the Bank since 2012 and has 30 years of experience in commercial and consumer banking. He is supported by a skilled and experienced team. Mr. Ali Raza Anjum is the Chief Operating Officer and has been with the Bank since 2012. He brings over 29 years of diverse experience in business, treasury, risk management, compliance, credit, internal audit, banking operations, finance, and human resources, having held senior management positions in prominent commercial and microfinance banks. Mr. Rizwan Maqsood serves as the Chief Financial Officer and also fulfills the roles of Company Secretary and General Counsel. With more than twenty years of extensive experience, he has managed a variety of functions including financial strategy, planning, management, reporting, analysis, accounting, auditing, and assurance. Mr. Junaed Rayaz, the Chief Risk Officer of the Bank, has almost 30 years of diverse experience in the banking industry, focusing on credit and market risk management, fraud prevention, and portfolio optimization.

Effectiveness

The Bank has designated various management committees to manage and oversee operational efficiency.

MIS

The Bank has implemented a robust Management Information System (MIS) infrastructure that features system-generated reports and detailed live dashboards to facilitate effective decision-making.

Risk Management framework

A dedicated risk management department regularly monitors credit, operational, and market risks, convening monthly to ensure adherence to the risk profile approved by the Board of Directors.

Technology Infrastructure

The Bank's IT infrastructure, which supports core banking and other essential systems, is located in a state-of-the-art data center at its Head Office. The Core Banking System (CBS) in

use is Oracle's Flexcube, which has been enhanced with features to address changing business needs and stringent regulatory requirements.

Business Risk

Industry Dynamics

The Microfinance Banking sector (" Sector ") continues to grapple with long-standing challenges in the form of declined asset quality, negative profitability and weakened Capital Adequacy Ratio (CAR) mainly driven by the historical impact of the COVID-19 pandemic in CY20 to the hazard of floods in Jul-Aug'22 followed by the economic slowdown in CY23 along with very high inflation in the past couple of years, the Sector's resilience has been repeatedly tested. During 6MCY24, the deposit base of MFBs increased by 6.7% to stand at PKR 637bln. The GLP of the Sector recorded a marginal uptick of 1.4% to stand at PKR 414bln. Whereas, the infection ratio jumped to 10.5% from 6.7% in CY23. The reported loss of the Sector soared to PKR 12.1bln from PKR 8.1bln in CY23. Consequently, the Sector 's equity base declined to PKR 22.6bln from PKR 37.4bln, resulting in the declined CAR of the Sector clocking in at 5.7% from 7.6% in CY23 falling far below the regulatory threshold of 15%. These factors cumulatively raise serious and persistent concerns about the performance of the Sector. Furthermore, during the year there was a significant credit crunch in South Punjab, coupled with intense wheat price crash, which adversely impacted the lending portfolio in the region.

Relative Position

HBL Microfinance Bank Limited is the leading Bank in the Sector with one of the highest share of deposits and gross loan portfolio (GLP) clocking in at 19% and 23% respectively.

Revenue

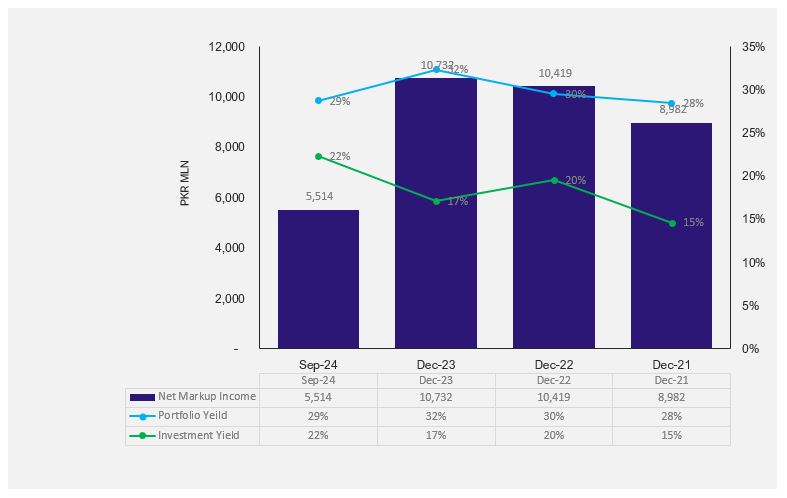

In CY23, the Bank's markup income rose by 38.1% to PKR 33.2bln (CY22: PKR 24.1bln 9MCY24: PKR 25.3bln) due to higher earnings from advances and investments. However, markup expenses surged by 65% to PKR 22.5bln (CY22: PKR 13.6bln) because of significant increase in policy rate from average of 13% in CY22 to average of 21% in CY23. Consequently, the Net Interest Margin (NIMR) increased slightly by 3% to PKR 10.7bln.

Profitability

Non-markup income grew 21% to PKR 2.5bln (CY22: PKR 2.1bln), mainly driven by fee and commission income of PKR 2.2bln. The provisioning charges increased to PKR 2.8bln (CY22: PKR 2.5bln). Due to high-cost deposits and administrative expenses, net profitability fell by 66% to PKR 405mln, impacting the CAR, which stood at 15.3% as of end-Dec23. Subsequently, in 9MCY24, the Bank reduced its advances by 6.1% to PKR 94.7bln. The Bank adjusted its funding mix by reducing costly deposits to control costs. Adopting IFRS-9 led to a 4x increase in provisioning expenses, reaching PKR 5.4bln. These factors, along with high-cost deposits and lower advances, resulted in a loss of PKR 4bln for 9MCY24. To address this, the Bank issued PKR 1.5bln Tier-II subordinated debt to various investors, while, the sponsor injected PKR 6bln in equity, raising the CAR to 16.1% by end-Sep24. With improved risk absorption capacity, the Bank plans to expand its advances, and lower funding costs are anticipated in a low-interest-rate environment, going forward.

Sustainability

HBL MfB has upgraded the Customer Origination System (LoS) to a Customer Management Solution (CMS) – an end-to-end digital model used to automate the processes and reduce

the turnaround time.

Financial Risk

Credit Risk

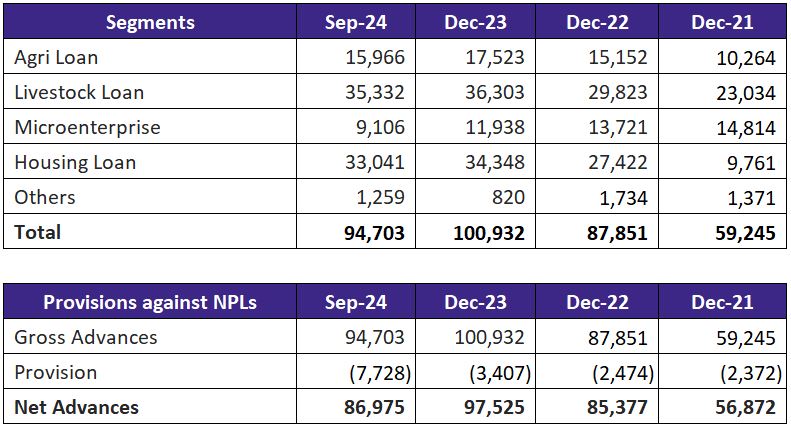

As of end-Dec23, gross advances rose by 14.9% to ~PKR 100.9bln (end-Dec22: PKR 87.9bln), with Non-Performing Loans (NPLs) increasing to PKR 2.7bln (Dec22: PKR 2.1bln), raising the infection ratio to 3% (Dec22: 2%). By end-Sep24, gross advances were reported at PKR 94.7bln, while NPLs climbed to PKR 9.5bln amid the wheat price crash, credit crunch in south punjab region, weather impacts and IFRS-9 adoption, pushing the infection ratio to 10%. While the write off was reported at PKR 2.8bln as of end Sep'24.

Market Risk

The Bank’s investment portfolio decreased by approximately 9% year-over-year to PKR 27.6bln at end-Dec23 (Dec22: PKR 30.4bln), primarily in government securities, though it increased to PKR 40.4bln by end-Sep24. The deposit base rose 10% year-over-year to PKR 128.2bln (end-Dec22: PKR 116.1bln), while total borrowings showed a modest rise, reaching PKR 9.3bln (end-Dec22: PKR 8.6bln).

Funding

The gross advances-to-deposit ratio (ADR) climbed to 76.1% (end-Dec22: 73.6%) due to the expanded advances portfolio for CY23. However, at end-Sep24, deposits stood at PKR 118.5bln, and total borrowings increased to PKR 13.7bln, with secured borrowings from financial institutions amounting to PKR 10.2bln, followed by subordinated debt at PKR 3.5bln.

Cashflows & Coverages

The Bank witnessed an improvement in its liquidity profile, as evident by the liquid assets to borrowings and deposits inclined to 44.7% at end-Sep24 (end-Dec23: 35.6%) driven by an increase in liquid investments.

Capital Adequacy

The Bank's equity base grew to PKR 14.2bln by end-Dec23 (end-Dec22: PKR 13.2bln, 9MCY24: PKR 15.7bln) due to sponsor capital injection and profitability, with a CAR of 15.3% (end-Dec22: 16.4%), meeting SBP’s minimum requirement. By end-Sep24, equity further strengthened to PKR 15.7bln, following an additional PKR 6bln from the sponsor, boosting the CAR to 16.1% and providing ample exposure capacity.

|