Profile

Legal Structure

Cherat Packaging Limited ("CPL" or "The Company") was incorporated as a public limited company in 1989. The Company is listed on PSX with a symbol of CPPL.

Background

Cherat Packaging Limited (CPL), part of the Ghulam Faruque Group, began producing paper sacks in 1992. It diversified into polypropylene bags in 2012, becoming a leading manufacturer of premium cement sacks, and ventured into flexible packaging in 2017.

Operations

The main business activities are manufacturing, marketing and sale of paper sacks, polypropylene bags and flexible packaging material. The plant has an annual production capacity of 420 million bags (kraft paper and polypropylene combined) and 19.8 mln Kgs of flexo and roto printing. The Company also exports cement bags.

Ownership

Ownership Structure

Cherat Packaging is part of the Ghulam Faruque Group. Faruque (Pvt.) Ltd holds 10.25% stake in Cherat Packaging Limited, followed by Atlas Insurance Limited 9.2%, Cherat

Cement Company Limited (7.35%), Greaves Pakistan Private Limited (5.02%), Mirpurkhas Sugar Mills Limited (4.97%).The Directors/other family members holds around 15%

stake of the company while the remaining stake is held by general public and other financial and non-financial institutions.

Stability

Since inception, Ghulam Faruque Group has continuously strengthened and diversified its lines of businesses.

Business Acumen

The sponsors have strong business acumen emanating from the groups established presence in cement, sugar,Chemical,paper and industrial Air conditioning and engineering sector. The diversified business lines provide a strong sense of stability as a group.

Financial Strength

Cherat Cement Company Limited reported net assets of ~PKR 25 billion, a turnover of ~PKR 38 billion, and a PAT of ~PKR 5.4 billion in FY24, providing strong support to the Company when required.

Governance

Board Structure

CPL’s Board of Directors (BoD) comprises 9 members which include 3 independent directors including a female representation on the board, 2 executive directors, and 4 non-executive.

Members’ Profile

Mr. Akbar Ali Pesnani, Chairman of the Baord, an MBA and fellow of both ICAP and ICMAP, has 48+ years of senior experience with the Aga Khan Development Network. He served as Chairman of Gwadar Port (2004–2006) and is currently Chairman of Aga Khan Cultural Service, Jubilee General Insurance, and Director at Cherat Cement and Pakistan Cables, with a 43-year association with the Ghulam Faruque Group. Mr. Aslam Faruque, non-executive director, a Marketing graduate, is CEO of Mirpurkhas Sugar Mills, Unicol, and UniEnergy, and a board member of Greaves Airconditioning and Greaves Engineering. Mr. Shehryar Faruque, non-executive director, a graduate of Davis & Elkins College, serves on the boards of Faruque (Pvt.) Ltd. and Zensoft (Pvt.) Ltd. He previously served as Director at NAFA and Summit Bank. Mr. Arif Faruque, non-executive director, a Swiss-qualified attorney with master's degrees in Law and Business Administration, is the CEO of Faruque (Pvt.) Ltd. He serves on the boards of Mirpurkhas Sugar Mills, Cherat Cement, and UniEnergy and is a member of the LUMS Board of Governors. Mr. Ali H. Shirazi, independent director, a Yale graduate, is Group Director Financial Services and CEO of Atlas Battery Ltd. He serves on the boards of multiple organizations, including Atlas Asset Management, Atlas Insurance, Shirazi Investments, National Foods, Cherat Packaging, Pakistan Cables, Atlas Foundation, Atlas Vocational Training Institute, National Management Foundation (LUMS sponsor), and Pakistan Society for Training and Development. Mr. Sher Afzal Mazari, independent director, a progressive agriculturist, focuses on sustainable farming and land management solutions. Previously, he had a 34-year corporate career spanning Chemicals, Foods, and FMCG industries. Ms. Maleeha Mimi Bangash, independent director, is a renowned banking and financial expert with over 26 years of experience in Singapore, Turkey, and Pakistan. Her diverse background includes roles in textile, telecommunications, banking, financial services, and investments.

Board Effectiveness

During the year, seven meetings of the Board of Directors were convened. The quality of discussion as captured in meeting minutes reflects high involvement of the board members in business activities. The two board committees namely: i)Audit Committee & ii) Human Recourse and Remuneration Committee. The Company has various policies in connection with Governance of Risk and Internal Control that have been approved by the Board of Directors and covered through different policies and disclosures.

provide assistance to the board on important matters.

Financial Transparency

EY Ford Rhodes Chartered Accountants are the external auditors of the Company. They have expressed an unqualified opinion on the financial statements for the period ending June 24.The Company has an in-house internal audit department, which reports to the Audit Committee.

Management

Organizational Structure

The Company has a well-developed organizational structure. The Company operates through two regional offices, located in Lahore and Islamabad,while its manufacturing facility is in Gadoon and a registered office located in Peshawar, reporting to the Head Office in Karachi. All the functional Heads report to the Company’s COO. The CFO and COO report to the CEO of the Company.

Management Team

Mr. Amer Faruque, CEO of the Company, holds a BS in Business Administration from Drake University. He serves on the boards of Mirpurkhas Sugar Mills, Faruque (Pvt.) Ltd., Greaves Pakistan, and Greaves CNG and is Executive Director Marketing at Cherat Cement. He previously served on the boards of GIK Institute, LUMS, and CIPE and is the Honorary Consul of Brazil in Peshawar. All functional departments are headed by seasoned professionals.

Effectiveness

Management’s effectiveness and efficiency can be ensured through the presence of management committees. There are no management committees in place, which indicates a room for improvement.

MIS

CPL’s manufacturing division is in KPK. The head office in Karachi, regional offices and manufacturing facility are integrated through single ERP platform. The Company uses SAP and customized software to generate various types of operational reports as required by the management in order to monitor the activities effectively.

Control Environment

The Company has an effective mechanism for identification, assessment and reporting of all types of risk arising out of the business operations. To ensure operational efficiency, the Company has an in-house internal audit department. The Audit Committee reviewed the resources and performance of the Internal Audit department to ensure that they were adequate for the planned scope of the Internal Audit function. Head of Internal Audit Department has direct access to the Audit Committee.

Business Risk

Industry Dynamics

Pakistan’s packaging industry consists of four major segments, paper, plastic, tinplate and glass. Paper and plastic segments occupy the major share in total market. CPL operates under paper and plastic segment of the Industry. The demand of paper segment is directly correlated with cement production and the demand of plastic segment is directly correlated with food & consumer products. The segment’s direct costs consist largely of imported raw materials. Therefore, volatility in exchange rates and international price trends has an impact on costs. For its Flexible Packaging Division (FPD), CPL also procures various raw materials locally, including inks, solvents, and films, ensuring efficient supply chain management.

Relative Position

There are five players including CPL, producing Paper bags and seven players, including CPL, producing PP bags. Major players in Paper bags are Nishat paper, Thal limited and Lahore Poly Industries, in PP bags are Ultra Packaging, Nova Synpac, Lahore Poly Industries and Syntronics. In Flexible packaging category, the key players are Packages Ltd, Kompass Pvt. Ltd, Kamil Packaging and Hamza Flexible. CPL is one of the largest player in the industry representing 15% of total market share in bags manufacturing segment.

Revenues

The operations are segmented in two main Divisions, i) Bags manufacturing Division (Paper bags and polyproplylene bags manufacturing) ii) Flexible

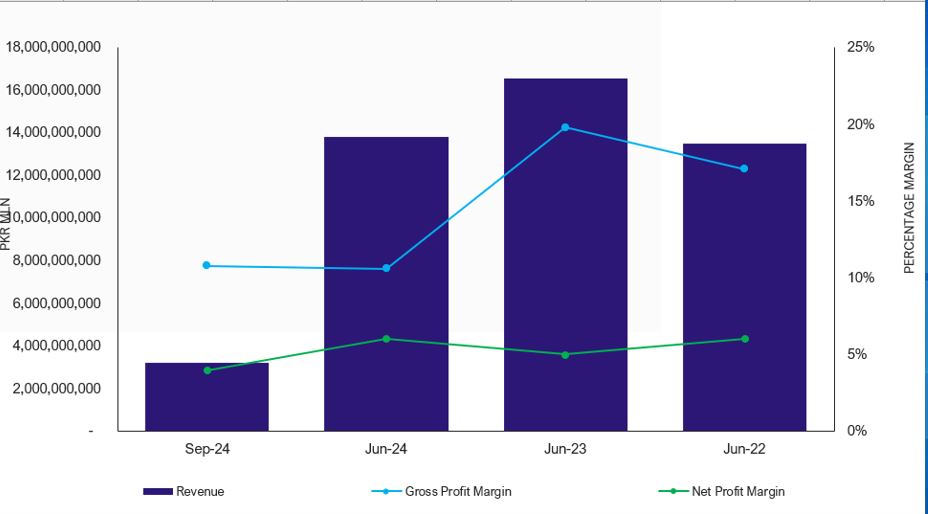

Packaging Division (Extrusion, Flexo Graphic and Rotogravure printing). The Company’s topline has shown a decline of 16.5% during FY24, the revenue stood at ~PKR 13.8bln. The Flexible Manufacturing Division has the largest share in revenue during FY 24, comprising above ~51% of total revenue.

Margins

The gross margins stood during FY24 at 11% (FY23: 20%). The operating margin stood during FY24 at 13% (FY23: 17%). The net profit margin is 6.41% in FY24 vs 5.5% in FY23 due to significant decrease in financing cost to ~PKR 838mln during FY24 vs ~PKR 1202mln in FY23 and disposal of KP Lines.

Sustainability

The revival of construction sector along with increase in cement demand will have a positive effect on the revenue of the Company. Further, the gross margins are expected to increase from current level with stable raw material cost. There is strong competition in the industry due to price sensitivity. To remain competitive the Company also plans to commission a Carrier/SOS bags unit by March 2025.

Financial Risk

Working capital

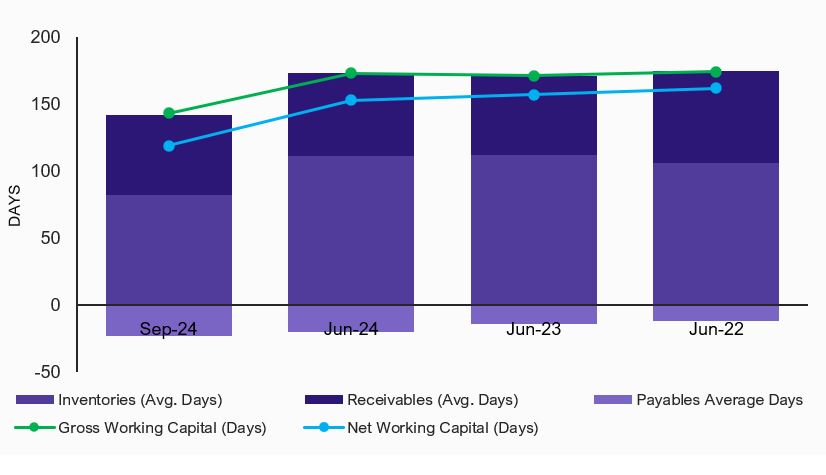

The cash cycle has increased slightly to 173 days during FY24 from 171 days during FY23, which is mainly triggered by increase in inventory days and decrease in receivable days. Majority of the Company’s sales are on credit as it’s the industry practice

Coverages

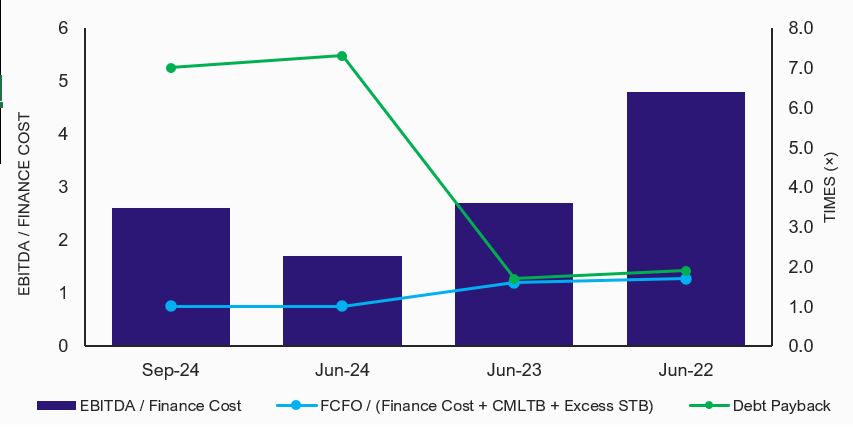

Total borrowings of the Company witnessed a decrease with short term borrowings comprised a significant portion of debt. Free cash flows from operations(FCFO) of the Company stood at PKR 1,187mln during FY24 (FY23: PKR~2,959mln)

Capitalization

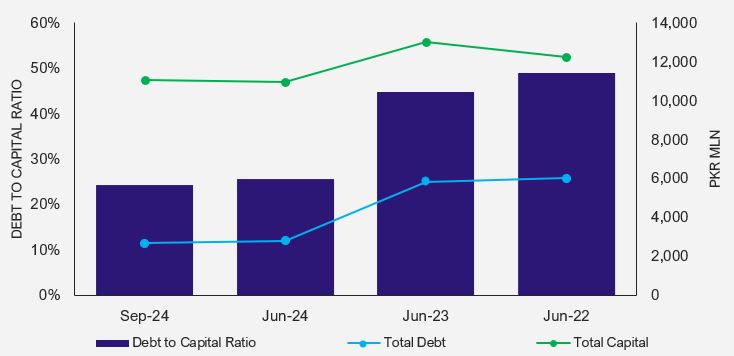

The capital structure of CPL is moderately leveraged. The leveraging stood at 25.6% at the end of FY24 (FY23: 44.7%). The significant decrease in short term borrowing over the year is attributable to effective working capital management.

|