Profile

Legal Structure

Dr. Ziauddin Hospital Trust (“the Trust” or “the Hospital” or "ZHT”) is registered under section 16-A of the Sindh Trust Act 2020.

Background

Dr. Ziauddin Memorial Hospital began in 1957 at Nazimabad, Karachi, when Sir Dr Ziauddin Ahmed’s daughter, Dr Aijaz Fatima (Late) and her husband Dr Tajamul Hussain (Late), established a 25-bed maternity home. This laid the foundation for the entire Dr. Ziauddin Group of Hospitals, one of the largest healthcare groups in the country. Dr. Ziauddin Hospital Trust was established in 1976 and the first campus opened in North Nazimabad, Karachi.

Operations

The Trust operates with four campuses: North Nazimabad Campus, Clifton Campus, Keamari Campus and Sukkur Campus. The hospital has a workforce of highly qualified doctors leading various departments. The Hospital currently operates in Karachi and Sukkur.

Ownership

Ownership Structure

The Hospital is in the ownership of the Trust and is run by the Board of Trustees.

Stability

The Trust has a well-defined trust deed that clearly specifies the tenure of the chief trustee and the mechanism for appointing a successor.

Business Acumen

Dr. Asim Hussain, Chairman of the Group, holds a portfolio of Chairperson Education City Board, Sindh. He also previously chaired Sindh Higher Education Commission, the National Reconstruction Bureau, and also served as Federal Minister Petroleum and Natural Resources. The Group prioritizes quality, transparency, and efficiency.

Financial Strength

The financial strength of the Group is primarily vested in the performance of Ziauddin Hospital Trust and Ziauddin University.

Governance

Board Structure

The Trust is governed by a six-member Board of Trustees. The Chief Trustee is Dr. Asim Hussain. The Board plays a vital role in ensuring effective oversight, decision-making, and in driving the Trust's operations and upholding best practices in their respective areas of focus.

Members’ Profile

The board members are highly qualified having considerable industry-specific exposure. The Board is dominated by Medical Professionals. Dr. Asim Hussain, is Chairman and Chief Trustee of ZHT and Chancellor of Ziauddin University. In recognition of his services to the nation in the fields of education and healthcare, he was conferred with the Sitara-i-Imtiaz and Nishan-e-Imtiaz.

Board Effectiveness

Board oversight is considered effective with board meetings held frequently on need basis.

Financial Transparency

BDO Ebrahim & Co., Chartered Accountants are the Company's external auditors. The audit of financial statements as of FY24 is in process. The auditors had issued an unqualified opinion on financial statements as of FY23. The auditors are listed on the SBP “A” category panel of auditors.

Management

Organizational Structure

The Hospital has a lean organizational structure as all departmental heads related to medical services are reportable to Medical Director and Campuses are managed by respective COOs. The internal committees are responsible for overseeing operations and conducting regular assessments of internal controls.

Management Team

Mr. Osama Ahmad, with over 20 years of diverse experience, has been associated with Ziauddin Hospital for the past 4 years. He currently serves as the Managing Director (MD) and Group Financial Advisor. Prior to this, he held prominent roles, including Director Finance at NUST Islamabad. Dr. Ashar Ekhlaq Ahmed (MRCP), the Medical Director of the Hospital, brings nearly two decades of expertise in the field of Rheumatology. The management team comprises qualified and experienced professionals committed to excellence in healthcare management.

Effectiveness

The departmental heads are responsible for their respective departments' operational activities and ensure the enforcement of SOPs required to maintain standards of quality. The management team has an adequate delegation of authority matrix.

MIS

The Hospital employs a Hospital Management System (HMIS) covering patient care aspects such as patient registration, ER, pharmacy and other relevant areas. Finance, billing, and supply chain are managed in Oracle ERP, fully integrated with HMIS. To ensure business continuity, security, integration and efficient operations, Hyper Converged Infrastructure (HCI) has also been installed including other I.T controls and applications.

Control Environment

The control environment is supplemented through a range of committees overseeing critical areas such as Hospital Management Committees, OT Management, AMS (Antimicrobial Stewardship), Monthly Coordination and Integration Committee. Further policies have been implemented in all important areas including Procurement Policy, HR Policy, Anti-Harassment Policy and Patient Complaint Procedures etc. Internal Audit Department has an ongoing role to assess the operational efficiency and mitigate the anomalies.

Business Risk

Industry Dynamics

According to data published by the Health Economic Survey of Pakistan as of 2023, the public sector operators with a capacity of ~1,284 hospitals, accompanied by 299,113 registered doctors and 151,661 units of beds. During FY24, the total federal health budget is ~PKR 25bln. As per the data available on PBS, the Medical equipment imports in Pakistan as of FY23 were PKR 124bln. The prime challenges specific to the private hospital industry are reputational risk followed by capacity and infrastructure development, ensuring the quality-of-care standards and managing the high cost of import coupled with escalated energy requirements.

Relative Position

The Hospital industry is highly fragmented. The ZHT consists of 845 beds reflecting an adequate market share in the hospital industry of Pakistan in terms of the total number of beds.

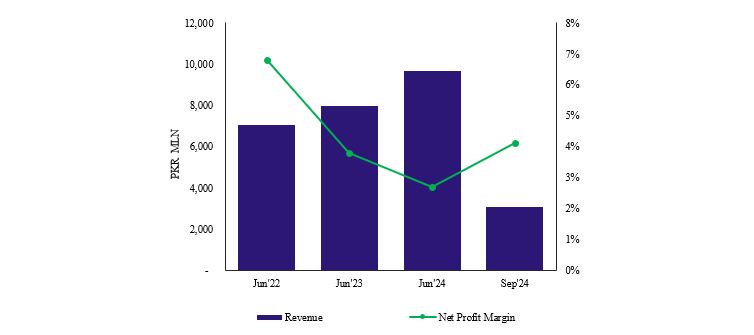

Revenues

During FY24, the top line of the Trust showed an increase of 21% YoY basis and stood at PKR 9.6bln (FY23: PKR 7.96bln, 1QFY25: PKR 3.06bln) mainly driven by the pharmacy store, followed by the laboratory, radiology etc. The top ten services contributed ~ 6.0bln in the topline. Majority of the revenue has been generated by the North Nazimabad branch followed by Clifton and Kemari, primarily driven by an increase in the number of patients treated annually and a moderate rise in treatment pricing. This aligns with the Trust's vision to provide healthcare services at affordable prices to the underprivileged segment of society. However, the core operations remain sustainable due to efficient cost management, increase in number of patients treated annually. While the Trust remains focused on its core mission of providing health services, it is actively enhancing its capabilities through balancing, modernization and replacement of biomedical equipment. Significant advancements in cancer treatment have been achieved, including the installation of a Cyclotron and the initiation of PET CT Scans, a states-of-the-art diagnostic tools to detect cancer across the body. Both have commenced commercial operations in the current year.

Margins

During FY24, the Trust generated a Profit after tax of PKR 258mln (FY23: PKR 305mln, 1QFY25: PKR 125mln). The net margin of ZHT showed a slight dip, primarily driven by inflated finance costs, a surge in the tax burden, and higher procurement costs of imported consumables (N.P Margin: FY24: 2.7%, FY23: 3.8%). While, during 1QFY25, the net profit margin increased to 4.1%. During 1QFY25, the gross profit margin of the Trust has shown an increasing trend.

Sustainability

The Trust had imported a Cyclotron and a PET-CT Scan for cancer detection in previous years. In the current year, these were successfully installed and commenced operations, enabling the production of isotopes for advanced diagnostics through PET CT Scans. Additionally, a new 180-bed facility in Sukkur has been operational since July 2024, with multiple phases gradually activated. The formal inauguration was held in December 2024, by the President of the Islamic Republic of Pakistan. The expansion of beds at the Clifton campus 5th floor is completed and has been operational. The Trust has installed solar of 350 kW at Clifton Campus and 510 kW at Kemari Campus, while 1 MW solar is being installed at Sukkur Campus to meet the energy requirements of the Trust. The management is dedicated to aligning the performance of the hospital with its financial projections.

Financial Risk

Working capital

The Trust aptly manages working capital requirements through short-term borrowings and internal cashflows. During FY24, the short-term trade leverage showed a decline, reflecting reduced room to borrow. The current ratio is 1.1x during FY24 (FY23: 1.4x, 1QFY25: 1.0x).

Coverages

The Trust's FCFO was PKR 982mln in FY24 (FY23: PKR 879mln, 1QFY25: PKR 403mln). The EBITDA / Finance Cost ratio stood at 2.8x during FY24 (FY23: 4.2x, 1QFY25: 3.7x).

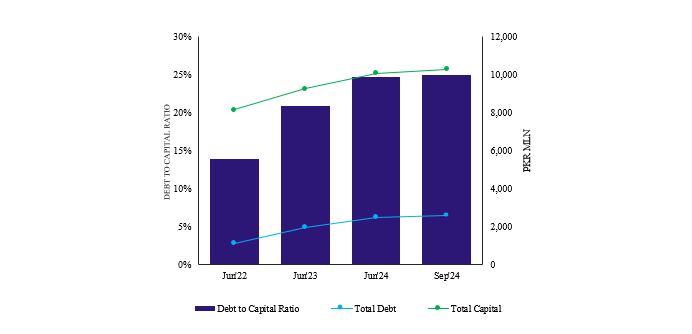

Capitalization

The Trust maintains a low leveraged capital structure, with leverage at 28.8% in FY24 (FY23: 25.5%, 1QFY25: 28.7%). In future, some change in leveraging is expected after the off-loading of debt, utilized for expansion. The borrowings are dominated by long-term borrowings which stood at PKR 1,501mln as of FY24 (1QFY25: PKR 1,530mln) . ZHT has short-term borrowings of PKR 444mln (1QFY25: PKR 491mln). The Trust has availed subsidized borrowing from SBP under the category of TERF and Refinance Facility for Combating COVID - 19 (RFCC). The equity base of the Trust stood at PKR 7.7bln mainly supplemented through an Unappropriated Profit of PKR 3.3bln during 1QFY25.

|