Profile

Legal Structure

Meko Demin Mills (Private). Limited ("the Company" or "MDML") operates as an unlisted, private limited Company under the Companies Act, 2017.

Background

The Company is a business venture of the Mekotex Group, incorporated on January 21, 2021. This incorporation marked a significant milestone with the strategic transfer of the denim business operations from Mekotex (Private) Limited to MDML, consolidating the Group's commitment to expansion and growth in the textile industry. Founded in 1979 by the late, Mr. Abdul Majid Qasim, the Mekotex Group has built a legacy of excellence in the textile sector. Over the years, the Group was guided by the visionary leadership of Mr. Abdul Majeed, who, along with his three sons—Mr. Khalid Majeed, Mr. Shoaib Majeed, and the late Mr. Ashraf Majeed—played an integral role in the Group's success and continued development.

Operations

The Company's operational capabilities span multiple stages of textile production, including spinning, weaving, dyeing, printing, and stitching. Its significant infrastructure features 44,000 spindles, 234 looms, 2,000 rotors, and 500 stitching machines. As part of its growth strategy, the Company significantly expanded its stitching unit located in the SITE area of Karachi, successfully achieving its targeted production capacity of 140,000 pieces per month.

The Company’s registered office is located at F-131 & 152, Hub River Road, SITE, Karachi, providing a strategic hub for its operations. The Company's day-to-day management is overseen by the founding family, with key responsibilities distributed among them: Mr. Shoaib Majeed leads the denim operations while Mr. Khalid Majeed heads the spinning, dyeing, printing, and processing sections.

To support its energy-intensive operations, the Company relies on an 8-megawatt power generation boiler, which efficiently meets its energy demands, ensuring smooth and uninterrupted production processes.

Ownership

Ownership Structure

The Company's entire shareholding rests with the sponsoring family, the Majeed family through individuals. The major stake of ~75% is held by Mr. Shoaib Majeed (55%) and his wife, Ms. Kiran Bano (20%). The remaining 25% stake is vested with his brother, Mr. Khalid Majeed.

Stability

The Company's ownership structure is expected to remain stable in the foreseeable future, with a clear and strategic transfer of shares to the next generation. The division of Group operations among the three brothers highlights the existence of a family constitution, ensuring the seamless continuation of leadership. The family-centric ownership, led by Mr. Shoaib Majeed, provides a hands-on approach and strong continuity, reinforcing the sponsor's long-term vision.

Business Acumen

Mr. Shoaib Majeed, the CEO of the Company, holds a degree in Business Administration and plays a pivotal role in overseeing multiple aspects of the family business. With his leadership, the Company continues to thrive under a hands-on approach. Mr. Khalid Majeed, an MBA graduate, serves as the Managing Director, where he is responsible for driving key areas such as business expansion, marketing, human resources, and other critical operations.

Financial Strength

The financial strength of the MDML emerges from the group's foothold divested in all aspects of the textile value chain. Apart from Meko Denim, the Group is operating in the local textile industry with two additional companies; Mekotex (Private). Limited and KAM International.

Governance

Board Structure

The Company's board comprises five members. The composition of the board includes three executive directors and two non-executive directors. The inclusion of an independent director will

strengthen the governance framework of the Company in line with the best governance practices.

Members’ Profile

Mr. Muhammad Khalid, the Executive Director of the Centre for Learning Law and Business (CLLB), brings over twenty-nine years of extensive experience. Mr. Farhan Ahmed holds a Master’s degree in Business Administration and has been associated with the Company for the past two years. Mr. Imran Motiwala, the CEO of AKD Investment Management Limited, offers a wealth of experience across various sectors. Mr. Muhammad Ahmed, the director of operations at MDML, holds a Bachelor's degree in Business Administration from York University, Canada. He joined the family business last year. The BOD members possess significant expertise, enabling them to offer valuable insights and contribute towards the strategic development.

Board Effectiveness

The Company does not have any formal board committees; relevant matters are presented directly to the BOD members for decision-making purposes.

Financial Transparency

To uphold high standards of transparency, Crowe Hussain Chaudhary & Co. Chartered Accountants have been appointed as the external auditors of the Company. They expressed an unqualified opinion on financial statements for the year ending on June 30, 2023. The firm is QCR-rated by the Institute of Chartered Accountants of Pakistan (ICAP) and is classified in Category 'A' by the State Bank of Pakistan (SBP) panel of auditors. The audit for the fiscal year 2024 is in process and is expected to be completed by the end of December 2024.

Management

Organizational Structure

The Company is structured into seven core departments to ensure a smooth flow of operations, each led by a strategic manager who directly reports to the BOD. These departments encompass both operational and support functions, ensuring comprehensive management across the business. The key operational departments include Marketing, Processing, Spinning, Weaving, Power, and Ginning, each responsible for essential aspects of the Company's production and business processes. The head office and finance departments are also integral parts of the organization, overseeing the Company's financial management and administrative functions. In addition to these primary departments, the Company has designated managers for Human Resources (HR) and Administration. These managers, while overseeing their respective areas, ensure alignment between administrative and financial functions.

Management Team

The Company's strategic managers, each with two decades of experience, contribute to the effective management of operations. The CEO, Mr. Shoaib Majeed completed his graduation in Business Administration and is vell-verse in the textile industry with an experience of over twenty-five years. He is supported by a team of highly qualified and skilled professionals. The CFO, Mr. Rehan Memon, an ACCA-certified professional, oversees financial intricacies and talent development.

Effectiveness

The management meetings led by the CEO, are scheduled on a need basis to discuss any operational matters. The overall effectiveness of management could be strengthened by formalizing the management committees.

MIS

For comprehensive reporting, the Company has implemented an Oracle-based ERP system with a strong emphasis on monitoring the performance of individual business segments. This performance data is regularly reviewed by the senior management to ensure effective oversight and timely decision-making.

Control Environment

The Company maintains an adequate control environment, supported by both in-house and international sales teams, manual quality control processes, and an established HSE (Health, Safety, and Environment) infrastructure.

Business Risk

Industry Dynamics

Textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%.

Relative Position

With a production capacity of 44,000 spindles, 234 looms, 2000 rotors, and 500 stitching machines, the Company is considered an emerging player in the local denim industry.

Revenues

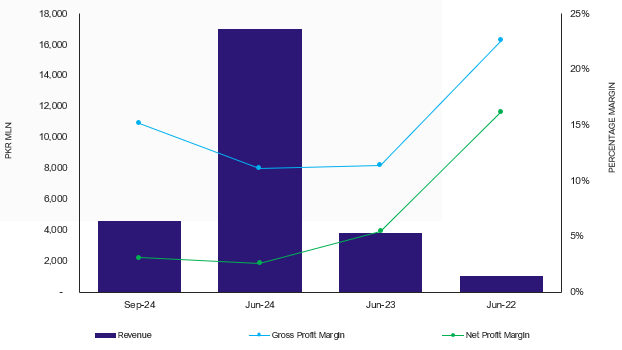

The Company's revenue base is predominantly vested in the sale of denim, garments and yarn. A tilt in the sales mix has been observed toward the local market to achieve long-term sustainability and cope with the evolving market trends in the global market. During FY24, the Company's top line experienced an upswing, reaching PKR 17.0bln (FY23: PKR 1.0bln), primarily due to a sizeable increase in local sales, which account for approximately 72% of the revenue, whereas exports make up around 28% (contribution of 78.8% from denim sales and 21.2% from garments). In terms of business contribution, denim products lead in terms of both, pricing and quantity. The MDML's top 10 client concentration remained at around 48%. Client concentration risk is considered moderate, attributed to the long-term association of the stable entities with the Mekotex Group. During 1QFY25, the Company's top line reached PKR 4.6bln (1QFY24: PKR 3.8bln), indicating a 20.1% growth on a quarter-on-quarter basis.

Margins

During FY24, the gross profit margin inched down to 11.1% (FY23: 11.4%) attributed to the procurement of raw cotton at a reasonable price and low energy cost backed by an operational 8-megawatt power generation boiler. PBIT exhibited a sizeable increase at PKR 1.4bln (FY23: PKR 82mln), despite elevated operating expenses of PKR 427mln (FY23: PKR 59mln) which is concomitant with the inflationary trends. The extensive working capital requirements magnified the Company's borrowing cost at PKR 796mln (FY23: PKR 13mln). The Company's bottom line was recorded as historically high at PKR 439mln (FY23: PKR 59mln), with a net profit margin of 2.6% (FY23: 5.5%). During 1QFY25, the Company's gross profit margin and operating profit margin showed an improvement at 15.2% (1QFY24: 11.6%) and 13.1% (1QFY24: 9.9%) respectively. However, the net profit margin slightly decreased to 3.1% (1QFY24: 5.7%) mainly due to elevated finance cost prevailing in the industry.

Sustainability

In FY24, the management successfully achieved its targeted production capacity of approximately 140,000 pieces per month. However, recognizing the risk posed by rising energy costs, the management intends to install a 9-megawatt wind turbine to mitigate the impact of elevated energy prices. Looking ahead, the management anticipates a robust year-on-year growth of approximately 17.0% in the Company's topline. However, the transition from the final tax regime to the normal tax regime for export-oriented units is anticipated to cause a modest reduction in the bottom line by the end of FY25.

Financial Risk

Working capital

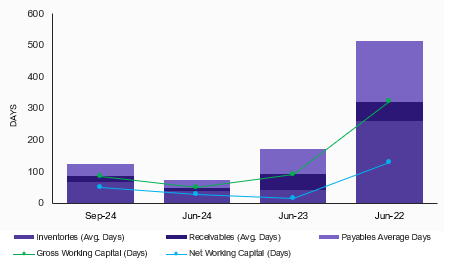

The Company's working capital cycle is a function of inventory days and trade receivables days for which the Company relies on internally generated cash flows and short-term borrowings. During 1QFY25, the net working capital cycle was stretched to 49 days (FY24: 27 days) attributed to a rise in the inventory cycle (1QFY25: 68 days; FY24: 38 days) and the trade receivable cycle (1QFY25: 19 days; FY24: 12 days), reflecting a delay in the collection of payments from the local customers. The Company holds a limited borrowing capacity as the short-term trade leverage was recorded negatively at 39% (FY24: -35.6%).

Coverages

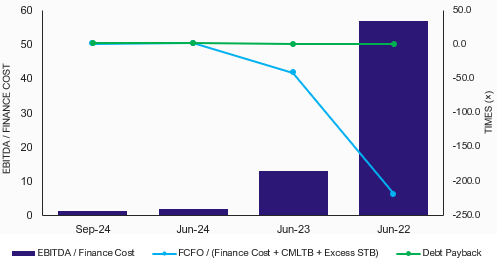

The dilution in PBT ultimately impacted the Company's Free Cash Flows from Operations (FCFO) reported at PKR 202mln (FY24: PKR 631mln). The expensive borrowings coupled with a dip in FCFO led to a slight decrease in the Company's interest coverage (1QFY25: 1.1x, FY24: 1.7x) and the core operating coverage (1QFY25: 0.8x, FY24: 0.9x). However, the improvement in the coverages of the Company remains imperative for the assigned ratings.

Capitalization

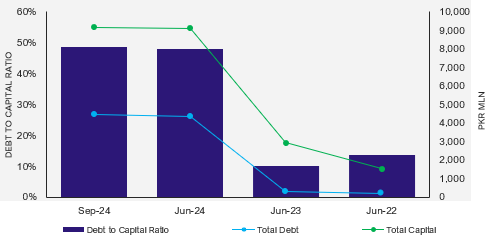

The Company's debt profile comprises a combination of related-party borrowings and short-term borrowings, which includes an Export Refinance Scheme (ERF) provided by the State Bank of Pakistan (SBP) as well as conventional borrowings. The Company secured long-term, interest-free loans amounting to PKR 3.5bln from its sponsors, specifically aimed at achieving the targeted production capacity. The Company has managed to maintain a leveraged capital structure mainly dominated by the STBs to meet the working capital requirements. During 1QFY25, the total leverage rose slightly to 48.5%, compared to 47.9% as of FY24. However, the Company’s equity base remained stable at PKR 4.7bln, with an unappropriated profit of PKR 650mln, demonstrating the Company's ability to maintain its financial position despite the higher borrowing levels.

|