Profile

Legal Structure

Sui Southern Gas Company Limited ("SSGC" or "the Company") is a public limited Company incorporated in Pakistan under the Companies Act, 2017 (repealed Companies Ordinance, 1984) and is listed on the Pakistan Stock Exchange. The registered office of the Company is situated at SSGC House, Sir Shah Muhammad Suleman Road, Block 14, Gulshan-e - Iqbal, Karachi. The meter manufacturing plant is situated at its' registered office.

Background

Starting with a humble beginning in 1954 as the Sui Transmission Gas Company, SSGC was officially established on March 30, 1989, through the merger of Karachi Gas Company, Indus Gas Company, and Sui Gas Transmission Company. Today SSGC is a pulsating powerhouse, committed to providing natural gas to its 3 million-plus customers in Sindh and Balochistan. Moreover, the Company also has two wholly owned subsidiaries, namely SSGC LPG (Pvt) Limited (SSL) and SSGC AE (Pvt) Limited (SSGC-AE). SSL is a fully integrated LPG marketing and distribution company capable of giving customers reliable and economic supply of product. The company's supply chain extends from allocation from local producers and a fully owned import terminal at Port Qasim to supply consumer retail packs of LPG. As such, activities of the Company start from the import of LPG and go on to the storage, bottling, distribution, and marketing of LPG, both in bulk tanks and cylinders. SSGC-AE continues to explore alternative energy sources that have been outside SSGC’s core business.

Operations

SSGC is Pakistan’s leading integrated public-limited large-scale natural gas utility Company. SSGC has been engaged in the business of transmission and distribution of natural gas, besides installation of high-pressure transmission and low-pressure distribution systems in the franchise provinces of Sindh and Balochistan, since 1954. Being a downstream company, the Company buys gas in bulk from more than twenty-four local and foreign Exploration and Production companies (E&P) for supply across its franchise areas. SSGC’s transmission system as of FY 23 comprises over 4,175 km of high-pressure pipeline ranging from 12" to 42" in diameter. The distribution activities covering over 160 cities and towns and 3,800 villages in Sindh and Balochistan are managed through its regional offices. SSGC operates its own meter manufacturing plant (MMP), established under license from M/s. Itron, France. The plant manufactures G-4 and G-1.6 meters for local consumption along with some exports to international buyers.

Ownership

Ownership Structure

The Government of Pakistan (GoP) holds a majority stake in the company, with 54% owned through the President of Pakistan and 7.25% held by the SSGC Employees Empowerment Trust. Public sector entities, including banks, development finance institutions (DFIs), insurance companies, non-banking finance companies, Takaful operators, and Modarabas, collectively account for 12.50% of the ownership. The remaining shares are distributed among mutual funds, directors, the general public, and other institutions.

Stability

As a public sector utility, SSGC and its pipeline network serve as strategic assets for the GoP. Given its critical importance and the scope of its operations, the government's majority ownership is anticipated to remain steady.

Business Acumen

Through two gas utility companies, SNGPL and SSGC, the GoP captures a significant combined share of ~79% in the total gas supply business in Pakistan. The Ministry of Petroleum (Petroleum Division) overlooks the portfolio of the government in the gas distribution business along with any formal policy development, while the Oil and Gas Regulatory Authority (OGRA) acts as a regulatory body.

Financial Strength

Given the strategic importance of the Company as an extension of the Government of Pakistan (GoP), it is anticipated that financial support will be provided during times of need. The GoP (Finance Division) has explicitly confirmed its commitment to extending the necessary financial assistance through a formal letter, ensuring the Company's ability to maintain its going concern status.

Governance

Board Structure

As of June 30, 2023, the board comprises ten members, including four Non Executive Directors, five Independent Directors and one Executive Director. The structure and appointment of the board of directors have been made in the best interests of the Company and in line with the standards of Corporate Governance.

Members’ Profile

The Board of Directors comprises accomplished professionals with diverse expertise. Dr. Shamshad Akhtar, the Chairperson, has over 40 years of experience in national and international development organizations, specializing in governance, privatization, and public-private partnerships. She also served as the Governor of the State Bank of Pakistan from 2006 to 2009.

The independent directors bring a wealth of expertise from various sectors. Mr. Muhammad Raziuddin Monem is a seasoned professional with over 40 years of experience in oilfield performance management, emphasizing QHSE and team building, and has collaborated with global energy giants like Exxon, Shell, and BP. Dr. Sohail Khan, a corporate strategy and business development consultant, has extensive international experience in the oil and gas sector. Mr. Ayaz Dawood, CEO of BRR Investments, is a distinguished entrepreneur and founder of several financial institutions, including Dawood Islamic Bank and Dawood Capital Management.

Government representation on the Board includes Mr. Shakeel Qadir Khan, Chief Secretary of Balochistan, who has extensive experience in financial management, disaster response, and institutional development. Ms. Saira Najeeb Ahmed, a senior civil servant, has expertise in economic policy, particularly in the power and petroleum sectors, and international development.

The non-executive directors further strengthen the Board. Mr. Shoaib Javed Hussain, Chairman of the State Life Insurance Corporation of Pakistan, has over 20 years of global experience in insurance, finance, audit, and risk management. Mr. Zafar Abbas, Additional Secretary (Policy) at the Ministry of Energy, is a seasoned civil servant with expertise in energy policy, international cooperation, and project management. Together, this distinguished team brings extensive experience and leadership to the organization.

Board Effectiveness

The board conducted 14 meetings during FY23 to discuss matters relating to the Company's operations. The presence of the members during the meetings remained satisfactory. Additionally, the Board has established five committees, namely the Board Human Resource and Remuneration Committee, the Board Finance and Procurement Committee, the Board Audit Committee, the Board Risk Management, Litigation, and HSE & QA Committee, and the Board Special Committee on UFG. The primary function of these committees is to assist the Board in the effective and efficient discharge of its functions and to provide feedback on matters of significant importance for the Board’s operations. The Board has approved Terms of Reference (ToR) for each of the committees to ensure that the interest of the Company is safeguarded. Each board committee also conducted regular meetings during the fiscal year to fulfill their respective roles.

Financial Transparency

SSGC, being a listed Company, adheres to the highest standards of Corporate Governance to ensure value, efficiency, and transparency in its business operations. As a public sector enterprise, the Company operates under a strong framework that includes the Public Sector Companies (Corporate Governance) Rules, 2013; the State-Owned Enterprises (Governance and Operations) Act, 2023; and the Code of Corporate Governance. M/s BDO Ebrahim & Co. are the external auditors of the company. The auditor gave a qualified opinion on the Company’s financial statements for the year ended June 30, 2023.

Management

Organizational Structure

The Company has a very comprehensive and streamlined organization structure comprising various divisions, including Transmission, Distribution, Human Resources, Coordination, Treasury & Finance, Construction, Procurement, Billing, Sales, Internal Audit, Customer Services, Technical Services, Planning & Development, Administrative Services, Billing, Risk Management, etc. Each division is further divided into sub-departments that each have specific responsibilities. Both the divisions and sub-divisions are headed by Senior General Managers (SGMs) and General Managers (GM) who are accompanied by a team of professionals. The SGM and GMs report to the Managing Directors and Deputy Managing Director Operations, who in return report directly to the Board.

Management Team

The management team consists of the Managing Director, Deputy Managing Director, Senior General Managers and General Managers who possess the required technical expertise and vast experience in the respective fields. Mr. Muhammad Amin Rajput is currently the Managing Director of SSGC. Previously, he had served as Chief Financial Officer and Chief Internal Auditor of the Company. Mr. Rajput has over 30 years of diversified experience in finance, audit, and management in the oil and gas, energy, manufacturing, and automobile sectors. Before joining SSGC, he served with K-Electric as its Chief Internal Auditor and Zahid Tractor, Saudi Arabia (Volvo and Caterpillar), in various senior finance and audit positions. Mr. Rajput is a Fellow Chartered Accountant (FCA) and Certified Internal Auditor. Syed Muhammad Saeed Rizvi is the Deputy Managing Director, Operations, and has been associated with the Company for over a decade. Previously he has held key positions in the Company including GM Meter Manufacturing Plant and SGM Engineering Services. An engineer by profession, he has extensive experience in Project Management, Product Quality, Product Development, Operations & Manufacturing.

Effectiveness

High-quality performance assessment and results-based accountability have been institutionalized to achieve better outcomes as per the expectations of the stakeholders. To achieve this, the management has implemented new performance-based assessment criteria backed by rigorous KPIs. streams, which include leadership, managerial, and technical programs, which have been instrumental in fostering a culture of continuous learning. Moreover, proper segregation of duties along with well-defined reporting lines and a hierarchical structure leads to smooth functioning, ensuring informed decision-making.

MIS

SSGC has deployed an Oracle e-Business Suite as its Enterprise Resource Planning (ERP) solution. In order to stay abreast of the latest technology, the Company upgraded its ERP solution from Oracle 11i to the Oracle R12 version. In addition, an Enterprise Project Portfolio Management solution was implemented in all gas distribution regions in Karachi using IBM Rational Focal Point software. The solution facilitates engineers in centralized management of the processes, methods, and techniques to analyze and collectively manage current and proposed gas distribution projects based on strategic value and controlling UFG characteristics. SSGC has a comprehensive Customer Care and Billing (CC&B) system to cater to the needs of customers in its franchise area. In the recent past, the Company upgraded its CC&B software through in-house functional enhancement to effectively resolve the current as well as future business requirements. The CC&B application is used for processing, reviewing, analyzing, billing, and raising claims on an individual customer through a centralized interface.

Control Environment

The Board has established a system of sound internal control to ensure compliance with the fundamental principles of probity and propriety, objectivity, integrity, and honesty, and relationships with the stakeholders, in the manner prescribed in the rules. The Company continued to enhance technological integration, using GIS and MAZIK platforms to maximize operations monitoring and network analysis capabilities. The GIS Platform integrates live data from rehabilitation projects and unauthorized gas usage, helping improve gas supply management and planning. Automated monitoring of customer usage was expanded, with 50 Town Border Stations (TBS) sites in Karachi, remotely controlled and monitored for greater operational efficiency.

Business Risk

Industry Dynamics

Pakistan's primary energy mix is dominated by fossil fuels, with natural gas and oil being the most widely used energy sources. The remaining natural gas reserves in the country (including non-pipeline quality gas) are estimated at 20.95 trillion cubic feet, making it the second-largest natural gas producer in South Asia. The total recoverable oil reserves in Pakistan are 249.05 million US barrels. Natural gas remains the dominant energy source in the country, comprising a substantial 41% of the total energy mix. In addition, imports of Liquefied Natural Gas (LNG) have increased and it now represents 11.4% of the overall primary energy supply. Total supply during 9MFY24 was recorded at ~20.8mln MT, registering a decline of ~1.4% YoY. Of this, local production formed ~78.3% (SPLY: ~78.7%), while the share of RLNG imports stood at ~21.7% (SPLY: ~21.3%) during the year. During the period, indigenous gas contributed ~9.3% (SPLY: ~11.6%) to the country’s power generation mix. Pakistan’s reliance on imported Re-gasified Liquified Natural Gas (RLNG) has traced an increasing trend over the recent years. During 9MFY24, RLNG imports rose ~15.0% YoY to ~6.9mln MT. During 9MFY24, the two gas utility companies (SNGPL & SSGCL) had laid a ~156Km gas transmission network, including ~3,614Km mains and ~76Km services lines. The two Government-owned gas utilities, SNGPL and SSGC, make up a significant combined share of ~79% (FY22: ~77.0%) in total gas supply across the country. Meanwhile, Independent systems comprise consumers having direct arrangements with gas-producing companies since they receive natural gas through dedicated pipelines or through virtual networks, including containers. In 7MFY24, total LPG extracted/processed was recorded at ~438,960MT up ~1.4% YoY (SPLY: ~432,801MT). Of the total, ~75.0% was extracted from natural gas fields, while the remaining ~25.0% was produced in refineries. During the time period, LPG production from refineries recorded a ~3.1% YoY increase, while LPG production from fields grew by ~0.9% YoY. In 7MFY24, LPG supply registered a ~3.3% YoY increase, recording at ~0.8mln MT, with local production and imports comprising ~56.5% and ~43.5%, respectively (SPLY: ~57.6% and ~42.4%, respectively).

Relative Position

The two Government-owned gas utilities, SNGPL and SSGC, have a significant combined share of ~70% in total gas supply to consumers in the Country. Meanwhile, Independent systems comprise consumers having direct arrangements with gas-producing companies since they receive natural gas through dedicated pipelines or through virtual networks, including containers. SSGC occupies a 21% share in the supply of gas to the Country, whereas SNGPL holds a 47% market share. However, SSGC is the main distributor in its franchise area of Sindh and Balochistan.

Revenues

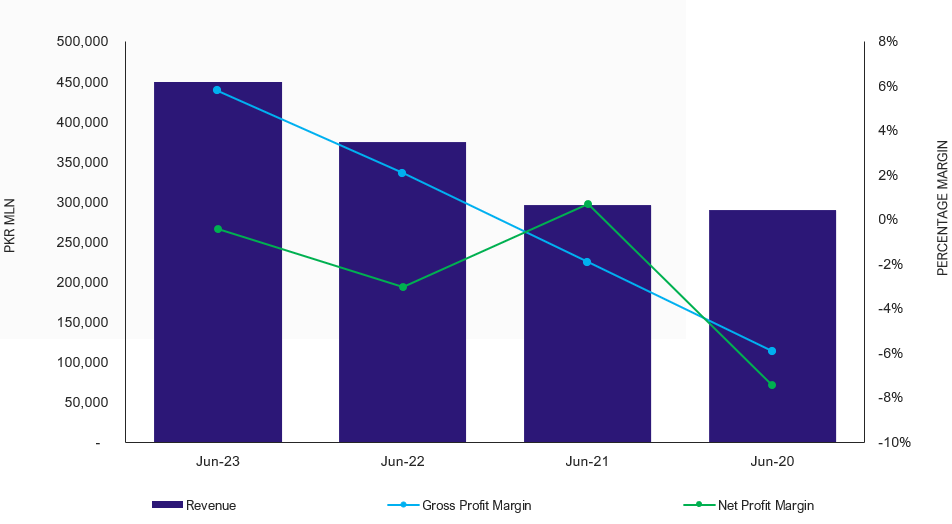

SSGC supplied 841 MMCFD of Gas including Natural Gas and RLNG during FY24 (FY23: 695MMCFD) to the consumers in different industries, including cement, fertilizer, power, and commercial, along with the domestic sector. During FY23, the Company recorded Net Revenues of PKR 449,501mln (FY22: 375,559mln) from the sale of Indigenous gas and RLNG net of taxes along with tariff adjustments on indigenous gas and RLNG which is a receivable from GoP under the provisions of license for transmission and distribution of natural gas granted to the Company by OGRA.

Margins

SSGC was allowed 23.45% (FY 2021-22: 16.60%) return on its average net operating fixed assets before financial charges and taxes. However, OGRA makes disallowances/ adjustments while determining the revenue requirements based on efficiency related benchmarks viz a viz Un-accounted for Gas (UFG), Human Resource Benchmark Cost, Provision for Doubtful Debts and some other expenses/ charges. These disallowances/ adjustments affect the bottom-line of the Company. In OGRA’s Determination on Final Revenue Requirements dated October 01, 2024 for FY 2022-23, SSGC was allowed a Return of PKR 23,496 million. Against the allowed return, OGRA made disallowances on account of UFG for Rs.27,679 million, PKR 254 million on account of Provision made against expected credit loss for the year in compliance of IFRS 9, Financial Instruments. However, SSGC successfully controlled HR Cost which remained under benchmark and accordingly PKR 836 million was allowed in bottom-line for saving in HR Cost. In addition, OGRA allowed SSGC prior periods claim of PKR 1,852 million on account of provision against expected credit losses, KMI Differentials and T&D Cost. As a result, Gross Margin witnessed significant improvement from 2.1% to 5.8% during FY23. However, due to rising finance cost of PKR 8,619mln along with higher UFG in the Balochistan region, the Company reported negative Net Margin of 0.4%.

Sustainability

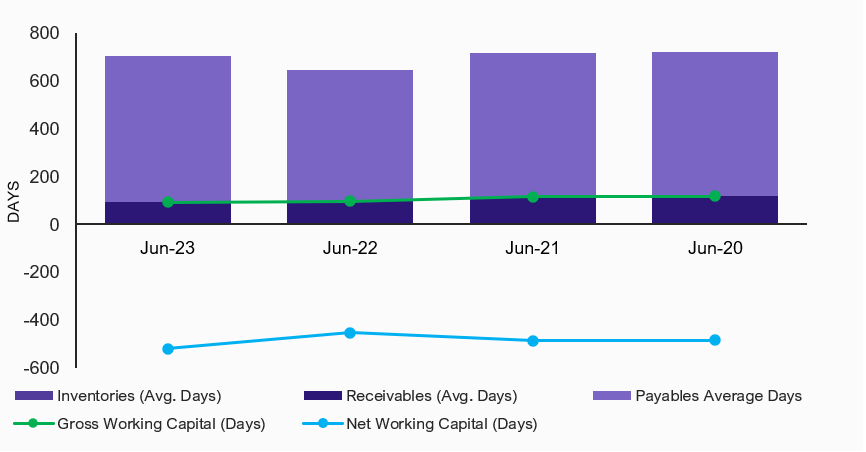

The Company has been undertaking extensive initiatives to improve its bottom line through vigorous and sustainable reduction in UFG. Company-wide UFG figures were reduced to 51.15 BCF against 59.99 BCF the previous year FY22, and the UFG percentage declined from 17.84% to 16.56%, reflecting an 8.84 BCF reduction and 1.28% decrease in UFG. In Karachi, an intense UFG reduction effort led to notable success, with a single-digit UFG percentage maintained from October 2022 until year-end, culminating in an annual UFG volume reduction of 7 BCF and a UFG percentage of 8.28% compared to 10.73% in the prior year. A comprehensive three-year plan has been developed to further optimize gas purchases in high-demand areas. In parallel, a master plan for Karachi will help improve pressure, reliability, and supply to industrial areas. Similarly, the Upper Sindh region achieved a 2.8 BCF reduction in UFG, with a UFG percentage decrease from 16.3% to 13.3% year-over-year. A three-year UFG Reduction Plan has also been implemented for Upper Sindh, focusing on strengthened operational controls and sustainable improvement. Balochistan remains a priority focus for UFG reduction, where weather and socio-economic conditions pose unique challenges. Although UFG levels remained at 25.9 BCF, the Company has rolled out an aggressive reduction plan aimed at saving 8 BCF in FY 2023-24. This initiative underscores SSGC’s dedication to achieving regulatory compliance and implementing long-term solutions in this region. To maintain a sound gas distribution network, especially in areas where infrastructure has reached the end of its useful life, a massive rehabilitation program has been initiated. Focusing primarily on Karachi and Upper Sindh, this program addresses system leakages and strengthens network integrity. As part of this effort, significant organizational adjustments have been made to optimize efficiency, resulting in doubled rehabilitation capacity over last year. This rehabilitation initiative is targeting 7,500 km of the network over the next three years.

Financial Risk

Working capital

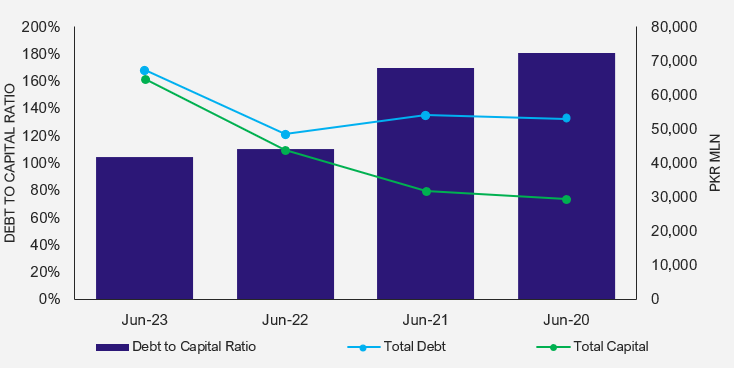

The Company is facing the situation of accumulated receivables from GoP and other government and non-government departments due to the overall circular debt situation. The Company has increased reliance on short-term borrowings of PKR 34,096mln, witnessing an increase over the years, obtained for working capital shortfall due to delay in tariff determination. In order to facilitate the operations, the GoP (Finance Division) has shown commitment to extend all support to meet its working capital requirements.

Coverages

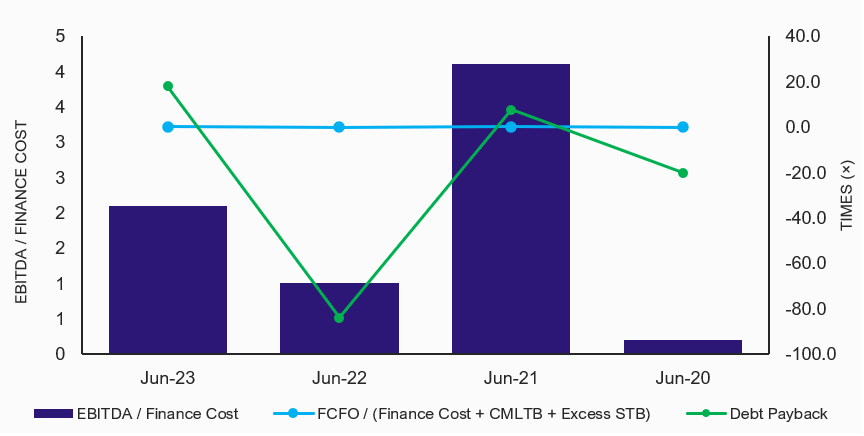

The Company incurred financial charges of PKR 8,619mln during FY23 in relation to its borrowings. During FY23, the Company's free cash flows from operations stood at PKR 16,760mln (FY22: 3,587mln). Hence, interest coverage (EBITDA/Finance Cost) and debt coverage (FCFO/Finance Cost) stood at 2.1x and 0.1x, respectively. Going forward, the borrowing is going to increase due to the rehabilitation plan in the coming years. The return on net assets received by the Company from OGRA will reflect the cost of borrowings in the tariff.

Capitalization

SSGC has obtained both long-term and short-term borrowings for capital expenditure and working capital shortfall. As of June 30, 2023, total borrowings of the Company stood at PKR 67,236mln witnessing a rise from the previous year. Loans under sovereign guarantee stood at PKR 16,333mln. The Company's leveraging ratio stood at 104.2% as on June 30, 2023, down from 110.2% at the end of the previous year. The slight improvement was due to the decline in losses during FY23. Furthermore, as of the end of Sep 2023, the Company’s equity has turned positive to PKR 1,497mln as a result of reported Net income of PKR 4,158mln during 1QFY24.

|