Profile

Legal Structure

US Apparel and Textiles (Private) Limited operates as a private limited Company. It was incorporated in Pakistan on February 18, 1987, under the Companies Ordinance, 1984 (now the Companies Act, 2017).

Background

US Apparel & Textiles (Private) Limited is the flagship business venture of the US (Umer-Siddique) Group.

Operations

The Company is principally engaged in the manufacturing and export of ready-made denim garments. The registered office of the Company is situated at 3-KM, Off

Defence I, Raiwind Road, Lahore. The Company's operational infrastructure includes five production units in Lahore.

Ownership

Ownership Structure

US Apparel is a wholly-owned subsidiary of AJ Holdings (Private) Limited; a prominent business venture of two sponsoring families (Mr. Mian Muhammad Ahsan & Mr. Javed Arshad Bhatti) of the US (Umer-Siddique) Group. The sponsors exercise their control over the Company’s board by virtue of its 100% stake in the Company.

Stability

The Group's ownership is divided between the two sponsoring families; Javed Arshad Bhatti and Mian Muhammad Ahsan. The Group’s holding Company, AJ Holdings (Private) Limited, primarily manages investments in subsidiaries and associated companies, which bodes well for the stability of the overall structure.

Business Acumen

US Group is one of the oldest business conglomerates in Pakistan with considerable interest in textiles. The group has developed quite good expertise in the textile garments sector, over the years, and enjoys long-term association with several customers abroad. The group’s presence has been limited to the textile sector but sustained volatility effectively over the years. Apart from the garment business, US Group also has a Denim weaving Mill namely, US Denim Mills Limited, involved in weaving. This has assisted the Company in expanding its operations despite challenging market dynamics.

Financial Strength

The Company’s affiliation with the US group demonstrates the strong financial muscle of the sponsors. According to the US Group Sustainability Report CY23, the group size is estimated at USD 356mln. The presence of the holding Company and the strong business profile of all group companies reflect the strong financial muscle of the sponsors. This indicates the sponsor's ability to support the flagship Company if needed.

Governance

Board Structure

The Company has a ten-member board with the presence of sponsors and their families. The inclusion of an independent director will strengthen the governance framework of the Company.

Members’ Profile

The board members possess significant business stature, with a proven track record of operations within the local textile industry. The sponsors bring a wealth of knowledge, backed by more than three decades of extensive experience, which has equipped them to navigate and thrive in a volatile market.

Board Effectiveness

Board meetings are held regularly, providing a platform for in-depth discussions on a wide range of critical aspects, including business strategy, operational performance, financial health, and market trends. These meetings are meticulously structured to ensure all relevant topics are thoroughly reviewed.

Financial Transparency

To maintain high standards of transparency, EY Ford Rhodes Chartered Accountants have been appointed as the external auditors of the Company, rated in "Category A" by the SBP panel of auditors. They expressed an unqualified opinion on the financial statements of the Company for the year ending June 30th, 2024.

Management

Organizational Structure

US Apparel is further divided into sub-business units. The sBU-USA and sBU-UK/EU have five garment manufacturing units with the capacity to produce 25 mln units annually. The manufacturing unit 2 & unit 5 fall under sBU USA and Units 1-R, Unit 3 & Unit 4 fall under sBU UK/EU. The manufacturing unit US Denim Mills, third sBU is a fabric mill that produces 40 mln meters of fabric annually. Each sBU is divided into functional departments, namely: (i) Finance & IT (F&I), (ii) Marketing, (iii) Production, (iv) Supply Chain and Corporate Sourcing (v) Admin & HR. All departments report to respective MD(s) who are responsible for delivering the bottom line and agreed goals & targets of SBU’s. MDs, CFO, Director Projects, Director HR, and Director IR report to the CEO designate.

Management Team

Mr. Hafiz Mustanser, the CEO designate, brings over two decades of professional experience and holds an MBA. He has been associated with the group since 1998. Mr. Uzair Ahmed, the CFO, is a qualified Chartered Accountant with more than 20 years of professional experience.

Effectiveness

The management meetings are held on a periodic basis with follow-up points to resolve or proactively address operational issues, if any, eventually ensuring a smooth flow of operations. These meetings are headed by the CEO.

MIS

The Company’s daily and monthly MIS comprises comprehensive performance reports which are reviewed frequently by the senior management. Recognizing the need for quality information systems to control and maintain the efficiency of operations, the Company has implemented an Oracle-based ERP solution - Oracle E-business suite, Harmony version 4.

Control Environment

US Apparel & Textiles utilize management systems as their mechanism for ensuring control. There is clear evidence of these systems being audited and certified externally. The Company has attained ISO 14001, 45001, 9001 SA8000, WRAP, Sedex, ISO 9001, OekoTex, GRS, RCS, OCS, SLCP light, STEP, CR 360, Higg FEM 3.0, and GOTS certification.

Business Risk

Industry Dynamics

The textile exports of the country reached USD 16.7bln in FY24, a slight increase from USD 16.5bln in the previous year, reflecting a growth of 0.93% YoY. The highest contribution came from the composite and garments segment at USD 9.1bln, followed by the weaving segment at USD 6.5bln and the spinning segment at USD 1.0bln. During 5MFY25, the textile exports stood at USD 7.6bln. In FY25, the transition from the final tax regime to the normal tax regime is set to impact the profitability matrix of export-oriented units, with a 29% tax on profits and a super tax of up to 10%. The consistent decline in policy rates over the last two quarters, along with the anticipation of further reductions, is expected to provide a cushion in the financial metrics of the industry.

Relative Position

US Apparel & Textiles (Private) Limited is recognized as one of Pakistan's leading textile exporters, ranking 10th among the top 100 textile exporters in the country during FY23–FY24.

Revenues

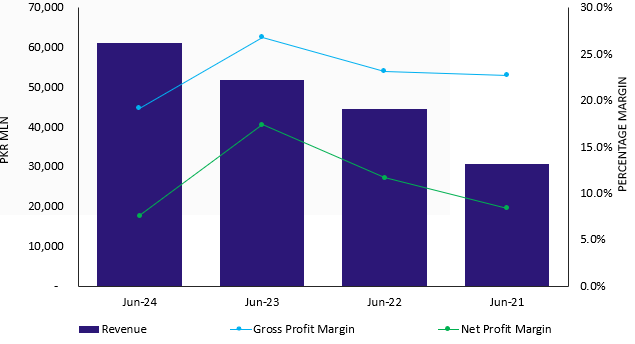

During FY24, the Company's topline experienced an upswing reaching PKR 61.1bln (FY23: PKR 51.9bln) reflecting a 3-year CAGR of 26.5% from June 2022 to June 2024. This growth was primarily fueled by a steady increase in business volumes over the years. A predominant portion of the Company's revenue base is generated through exports (FY24: PKR 60.6bln; FY23: PKR 51.5bln), which account for 98.6% of the total sales, followed by a minimal contribution from local sales. The Company has established a stable clientele around the globe. United States is the Company's prime export destination followed by United Kingdom and Europe. The client concentration risk is considered moderate supported by a long-standing association of the Company with well-established entities.

Margins

The removal of energy tariff subsidies, rising inflation, revision of the minimum wage rate, and stability in the USD exchange rate have been key factors impacting the Company's cost structure, leading to a dilution in profitability. Despite these challenges, the Company is still able to generate a reasonable profit after tax of PKR 4.67bln in FY24 (FY23: PKR 9.03bln). During FY24, the Company reported a gross profit of PKR 11,735mln (FY23: PKR 13,932mln), with a gross profit margin of 19.2% (FY23: 26.8%) and a net profit margin of 7.6% (FY23: 17.4%).

Sustainability

In FY24, the Company enhanced its overall production capacity by 15,000 pieces per day. This will cater to expansion in the revenue base and strengthen the business profile of the Company.

Financial Risk

Working capital

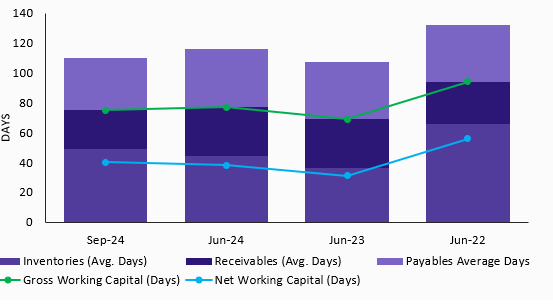

The Company prioritizes financing its working capital requirements through internally generated cash flows. The net working capital cycle stood at 40 days (FY23: 38 days) attributed to an uptick in the inventory cycle. The Company maintained a strong liquidity profile with a current ratio of 2.8x (FY23: 2.7x) during the period under review.

Coverages

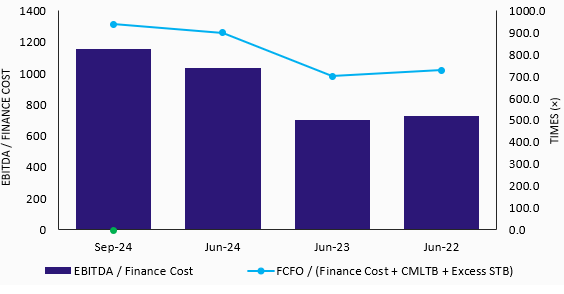

In FY24, the dilution in profit before tax resulted in a decline in the Company's Free Cash Flows from Operations (FCFO) clocking at PKR 6.6bln (FY23: PKR 9.9bln). However, the Company’s solid financial coverage is noteworthy, particularly given its debt-free position. Resultantly, the Company's interest coverage and core operating coverage were recorded in a comfortable range.

Capitalization

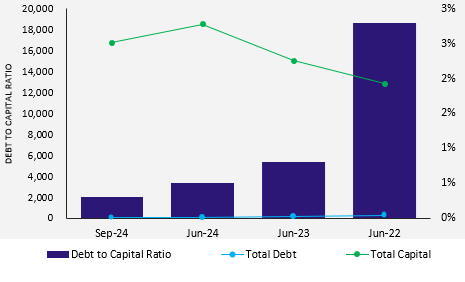

The Company fortifies its financial structure through a stalwart equity position of PKR 16.6bln (FY23: PKR 18.3bln). The equity of the Company is slightly reduced due to the payment of interim dividend. The Company has no short-term borrowings and has secured an interest-free loan from its holding Company to support its net working capital requirements. The Company has only availed non-funded credit facilities from banks for trade purposes.

|